Last updated: June 2026 · Reviewed by Pascal Burke, Licensed Insurance Broker (CA #6015321, TX #3305690)

In short: General liability insurance for contractors is a third-party policy that pays for bodily injury, property damage, personal and advertising injury, and legal defense costs that come out of your work. Most contractors pay $150 to $400 per month ($1,800 to $4,800 per year) for a standard $1M per occurrence / $2M aggregate policy, though roofing, structural, and high-revenue operations often pay more. The $1M/$2M limit is the baseline most bids, leases, and vendor portals ask for. You usually need it the moment a contract, a general contractor, or a city permit packet asks for a Certificate of Insurance. Get a quote or request a COI and we will help you move fast.

What general liability insurance covers (and what it does not)

In brief: General liability covers third-party bodily injury, third-party property damage, personal and advertising injury, and legal defense costs. It does not cover your own employees, your own tools, your own vehicles, or your own workmanship.

General liability (GL) is built around claims from people and property that are not yours. If your operations injure a member of the public or damage someone else's property, GL is the policy that responds. It is the coverage general contractors, project owners, and vendor portals look for first, and it is the policy a Certificate of Insurance usually proves.

Core coverages most contractors recognize

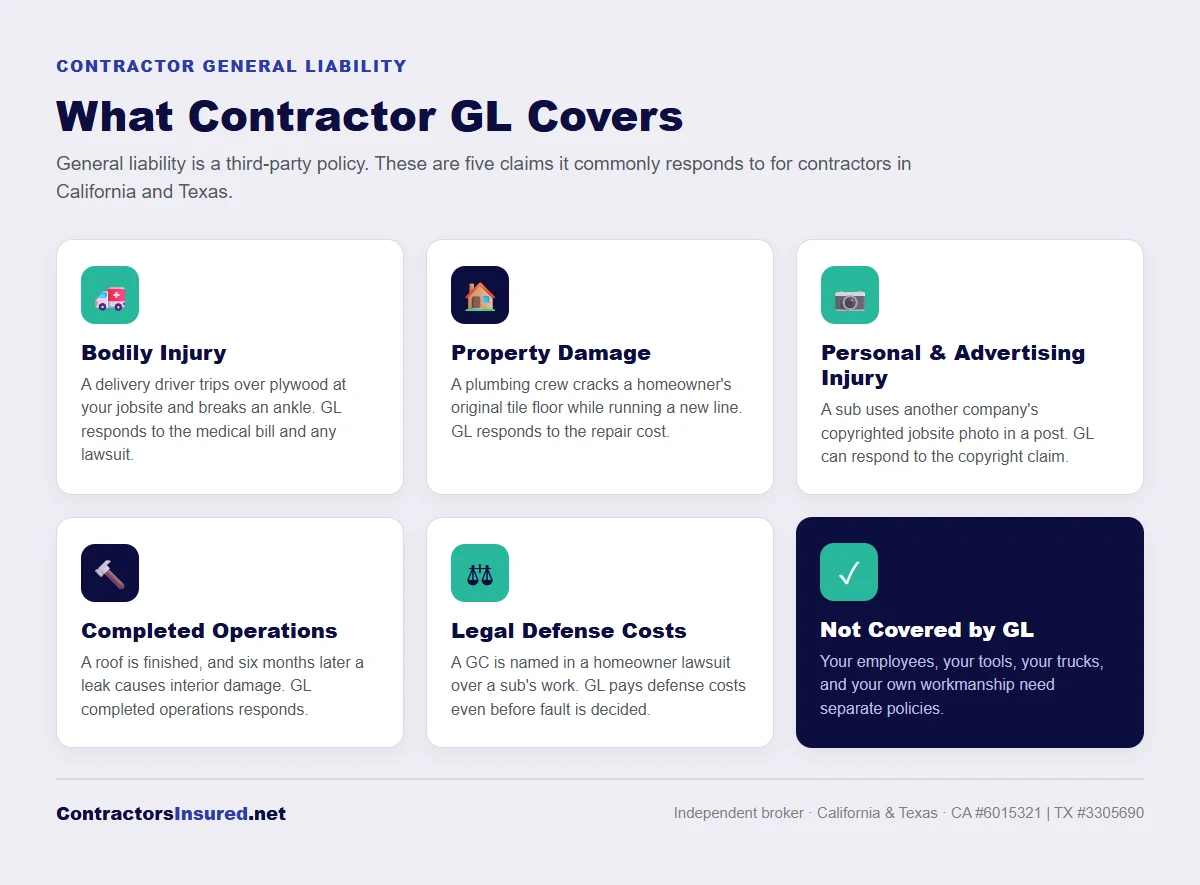

- Third-party bodily injury: medical bills and legal liability when your work injures someone who is not your employee.

- Third-party property damage: repair or replacement when your operations damage property that belongs to a client or another party.

- Products and completed operations: claims that show up after a job is finished, tied to the work you completed.

- Personal and advertising injury: claims like libel, slander, or copyright issues in your marketing.

- Legal defense costs: attorney fees and defense expenses, which a GL policy often pays even when a claim turns out to be groundless.

Five real contractor scenarios general liability responds to

Bodily injury, third-party visitor

A delivery driver dropping materials at your jobsite trips over a stack of plywood and breaks an ankle. GL responds to the medical bill and any lawsuit that follows.

Property damage, client property

A plumbing crew on a remodel accidentally cracks the homeowner's original tile floor while running a new line. GL responds to the repair cost.

Personal and advertising injury

A subcontractor uses a copyrighted jobsite photo from another company in their own social media post. GL can respond to the resulting copyright claim.

Completed operations, post-job claim

A roofing crew finishes a project, and six months later a leak causes interior damage at the same address. GL completed operations responds.

Defense costs, even if you are not at fault

A general contractor is named in a lawsuit by a homeowner over a subcontractor's work. GL pays defense costs even before a determination of fault.

What general liability usually does NOT cover

GL is narrow on purpose. It does not pay for injuries to your own crew, damage to your own tools, accidents in your own trucks, or mistakes in your own workmanship. Those exposures need their own policies: workers' compensation for employee injuries, commercial auto for vehicles, tools and equipment (inland marine) coverage for your gear, and professional liability (E&O) for design and consulting errors.

Who actually needs contractor general liability insurance

In brief: Most contractors need GL because contracts, leases, GCs, vendor portals, city permit packets, and project owners commonly require it before work begins. State law typically does not require GL for every business, but it is effectively required by the contracts and packets contractors work under every day.

If you bid work, sign with a general contractor, lease a yard or shop, or pull permits in a major city, you will almost certainly be asked for a Certificate of Insurance that shows general liability. That is true for general contractors, roofers, plumbers, HVAC and electrical contractors, finish trades, handymen, and specialty contractors alike.

It is worth being precise about the legal picture. In California, the Contractors State License Board (CSLB) is focused on workers' compensation for licensees and proof of insurance in many bidding contexts, not a blanket GL mandate. In Texas, there is no statewide license board that mandates GL for every contractor. So GL is rarely "required by state law" in the blanket sense. Instead, it is required by the contracts, leases, GCs, vendor portals, and city permit packets you encounter on nearly every job. The practical result is the same: no GL, no work.

If you work across both states, our California general contractor general liability and Texas general contractor general liability pages go deeper on each state's contract and COI patterns.

How much does general liability insurance cost for contractors

Most contractors pay $150 to $400 per month ($1,800 to $4,800 per year) for a standard $1M per occurrence / $2M aggregate general liability policy, with roofing, structural, and high-revenue operations often paying more.

In brief: Cost varies by trade, revenue, payroll, claims, subcontractor usage, and contract limits. Below are typical 2026 ranges for California and Texas contractors, plus a comparison to the broader small-business range you see in national aggregator quotes.

Two contractors with the same $1M/$2M limit can pay very different premiums. A handyman doing light repairs and a roofing contractor working at height carry different severity risk, so carriers price them differently. The tables below show where most contractors land. Final pricing depends on underwriting.

Average general liability cost by business type

| Business type | Monthly range | Annual range | Why this tier |

|---|---|---|---|

| Low-risk consultant / office business | $40–$150 | $480–$1,800 | Limited public interaction, no jobsites |

| Retail or customer-facing business | $60–$200 | $720–$2,400 | Foot traffic, slip-and-fall exposure |

| Specialty contractor (light trade) | $75–$225 | $900–$2,700 | Smaller projects, lower payroll |

| General contractor | $150–$400+ | $1,800–$4,800+ | Subcontractor risk, completed operations |

| Roofing or high-hazard contractor | $250–$700+ | $3,000–$8,400+ | Heights, hot work, severity claims |

Contractor general liability cost by trade (2026)

| Trade | Typical monthly | Typical annual | Top underwriting concern |

|---|---|---|---|

| General contractor | $150–$400 | $1,800–$4,800 | Subcontractor coverage continuity |

| Roofing contractor | $250–$700+ | $3,000–$8,400+ | Heights, hot work, completed operations |

| Plumbing contractor | $125–$350 | $1,500–$4,200 | Water damage severity |

| HVAC / electrical | $125–$325 | $1,500–$3,900 | Property damage, hot work |

| Finish trade (paint, drywall, flooring) | $75–$200 | $900–$2,400 | Smaller claims frequency |

| Handyman / light repair | $50–$175 | $600–$2,100 | Limited scope contracts |

Unlike national aggregators that quote a $40 to $150 per month range for a generic small business, contractor general liability typically lands between $150 and $400+ per month because jobsite work involves property damage exposure, completed operations, and subcontractor risk that office businesses do not face. When you see a very low online quote, check whether it was rated for a contractor class at all, or for a generic office business.

For city-level numbers, see our metro cost guides for Los Angeles, San Diego, Dallas, Houston, Austin, Fort Worth, and San Antonio. More California and Texas metro guides are on the way. Ready for a real number? Get a quote.

Why contractor GL costs more than business GL

In brief: Contractor work creates property damage, bodily injury, and completed-operations exposure that office and consulting businesses do not. That risk profile makes carriers price contractor policies higher even at the same coverage limit.

An accountant's liability risk is mostly someone slipping in a waiting room. A contractor's risk is spread across active jobsites, heavy materials, power tools, work at height, and the property of other people. Several factors push contractor GL above office-business GL:

- Jobsite injury risk: the public, delivery drivers, and other trades move through active sites.

- Property damage to client property: you work inside and around property you do not own.

- Completed-operations tail: a claim can surface months after the job is done.

- Subcontractor risk transfer: if subs are not properly insured, their exposure can fall back on you.

- High-value project liability: larger projects mean larger potential losses.

- Contract-driven endorsements: requirements like Additional Insured, Primary & Noncontributory, and Waiver of Subrogation broaden the carrier's exposure.

The difference is easiest to see on the jobsite-injury line. An office business mostly worries about a visitor tripping in a lobby. A contractor is responsible for a constantly changing environment where homeowners, delivery drivers, building inspectors, and other trades all move through the same space while power tools run and materials are staged overhead. A single dropped tool, an unmarked trench, or a load that shifts on a forklift can injure someone who has nothing to do with your crew, and the resulting third-party claim is exactly what general liability is built to absorb. Carriers price that constant, mobile exposure into the base rate, which is why a contractor and an accountant with identical revenue rarely pay the same premium.

The completed-operations tail is the part contractors most often underestimate. Unlike a retail slip-and-fall that happens while the business is open, a construction defect can surface months or even years after the crew has packed up, when a roof starts leaking, a deck pulls away from a wall, or a slab cracks. Your policy generally needs to respond based on when the damage appears, not when the work was performed, so carriers reserve for claims that may not arrive until long after the premium was collected. That long liability horizon is a real cost, and it is one of the main reasons a roofer or framer pays more than a low-risk handyman even at the same coverage limit.

Subcontractor risk transfer pushes the number in the other direction, for better or worse. If you hire subs and collect their Certificates of Insurance with proper Additional Insured and Waiver of Subrogation endorsements, you move a meaningful share of the risk onto their policies, and a well-documented program can actually keep your rate in check at audit. If you cannot prove your subs were insured, the carrier treats their payroll as if it were yours, your audit bill climbs, and an uninsured sub's accident can land squarely on your general liability. The paperwork is not bureaucracy for its own sake; it is the difference between a clean renewal and a surprise premium charge.

All of this is why a contractor should treat a surprisingly cheap online quote as a question rather than a bargain. A rate that looks like office-business pricing was often generated against a generic class code that does not match real construction operations, and a misclassified policy can leave gaps that only show up when a claim is denied or a general contractor rejects your COI for the wrong wording. The goal is not the lowest sticker price; it is a policy rated for what you actually do, with the limits and endorsements your contracts demand. That is the part an independent broker is built to get right the first time.

Cost by coverage limit

In brief: $1M per occurrence / $2M aggregate is the most common contractor baseline. Many commercial, public, and high-value projects require $2M/$4M or push to umbrella and excess for the additional limit.

Your contract usually dictates the limit, not your preference. Most bids and leases ask for $1M/$2M. Larger and public projects often ask for more, which is frequently built by stacking an umbrella or excess policy over your underlying GL rather than buying a single very high limit.

| Limit | Common use case | Notes |

|---|---|---|

| $1M / $2M | Default for most contractor bids, leases, and vendor portals | The most common requirement |

| $2M / $4M | Larger commercial, multi-family, certain public projects | Often satisfied by combining $1M GL + $1M umbrella |

| $5M+ via umbrella/excess | Tech campus pre-qualification, transit, hospital, government | Built by stacking umbrella over the underlying GL |

| Project-specific | Per-contract requirements | Read the bid packet carefully; mismatches cause COI rejections |

The 7 factors carriers use to price your contractor GL policy

In brief: Carriers underwrite contractor GL on seven main inputs. Knowing them helps you prepare a quote packet that prices accurately the first time.

- Trade or class code: your actual operations set the base rate.

- Annual revenue: premium scales with how much work you do.

- Payroll and employee count: drives both GL and workers' compensation exposure.

- Subcontractor usage and documentation: how much you sub out, and how well subs are vetted.

- Claims history: past losses predict future ones.

- Coverage limits and endorsements requested: contract-driven additions broaden coverage.

- Carrier appetite and jobsite geography: where you work and which carriers want your class.

| Factor | Why it matters | What to prepare |

|---|---|---|

| Trade / class code | Determines base rate | Be specific about your actual operations |

| Annual revenue | Premium scales with revenue | Last full year + projected current year |

| Payroll & headcount | Workers' comp + GL exposure | W-2 vs 1099 mix, employee count |

| Subcontractor usage | Risk transfer adequacy | What % of revenue, how they are vetted |

| Claims history | Past = predictor of future | 5 years of loss runs from prior carriers |

| Limits & endorsements | Contract-driven | Bid packet COI requirements |

| Job geography | Risk concentration | Counties and project types |

For more on how class codes and audits shape your final number, see contractor class codes and premium audit.

Local contract and COI requirements in California and Texas

In brief: California contractors regularly face CSLB workers' comp requirements and city procurement insurance schedules. Texas contractors face TDI-published policy guidance and city and county vendor packets that commonly require $1M per occurrence and $2M aggregate plus Additional Insured language.

These are examples of how requirements show up in practice, not a universal state mandate. The exact wording always comes from your specific contract or permit packet.

California examples. The City of Los Angeles, through its Bureau of Engineering insurance requirements, commonly requires a $1M/$2M general liability baseline for contracted work, and the published schedule spells out the exact limits and endorsement language a contractor must carry before the city will execute an agreement. The City of San Diego likewise publishes its vendor insurance and bond requirements for contractors doing city work, so you can confirm the limits before you bid rather than after the award. Statewide, the Contractors State License Board (CSLB) workers' compensation rules require coverage for licensees in most situations even with a single employee, and roofing contractors must carry it regardless of whether they have any employees at all. A Certificate of Insurance is how you prove all of this.

Texas examples. The Texas Department of Insurance (TDI) publishes a plain-language commercial general liability explainer that mirrors the coverage described on this page, which is a useful neutral reference when a client or general contractor questions what your policy actually does. At the city level, Dallas City Code Section 43-170 is a clear municipal example that references a $1M per occurrence and $2M aggregate CGL standard with Additional Insured and Waiver of Subrogation wording. Austin and San Antonio publish venue and vendor insurance packets with similar schedules. If you sub out work, plan for subcontractor insurance compliance up front so a missing sub COI does not stall your own billing.

What general liability does NOT cover (and the policies that fill those gaps)

In brief: GL is a third-party policy. It does not cover your employees, your trucks, your tools, your design errors, or pollution. Each of those exposures needs its own policy.

- Workers' compensation for injuries to your employees.

- Commercial auto for your trucks and vans.

- Tools and equipment (inland marine) for your gear on the move.

- Professional liability (E&O) for design and consulting errors.

- Builder's risk for work-in-progress property.

- Umbrella and excess for higher limits above your GL.

- Contractor bonds for license and project bond requirements.

- Ghost policy as a no-employee workers' comp solution when a contract still demands a WC certificate.

How to lower your contractor GL cost without creating coverage gaps

In brief: The fastest way to lower premium is to be accurate (trade class, revenue, payroll, subs) and clean (no preventable claims, no coverage gaps, documented sub vetting). Cheap is not the same as competitively priced.

Most of the savings on a contractor GL policy come from how you present the risk, not from buying less coverage. The levers that actually help:

- Use an accurate class code: the right contractor class code avoids both overcharging and audit surprises.

- Keep a clean claims history: preventable claims raise rates for years.

- Document subcontractor vetting: collect sub COIs and meet subcontractor insurance compliance standards so their exposure is not rated as yours.

- Report revenue and payroll accurately: under-reporting backfires at premium audit.

- Bundle where it makes sense: a business owner's policy can be efficient for lower-risk classes.

- Avoid lapses: a coverage gap is a red flag to the next carrier.

- Read bid packets before binding: so required endorsements are quoted correctly the first time.

What to prepare before requesting a contractor GL quote

In brief: A complete quote packet gets a same-day or next-business-day quote. Missing items add days of back-and-forth and sometimes push the policy to a less-competitive market.

| Information needed | Why your broker needs it |

|---|---|

| Legal business name + DBA | For policy issuance + COI accuracy |

| Trade and detailed scope of work | Drives class code selection |

| Business address + job geography | Carrier rating + appetite |

| Annual revenue (last + projected) | Premium base |

| Payroll + employee count + W-2/1099 split | GL + WC exposure |

| Subcontractor percentage and vetting process | Risk transfer adequacy |

| 5-year claims history (loss runs from prior carriers) | Underwriting fit |

| Desired limits (per occurrence + aggregate) | Contract requirement match |

| COI / endorsement wording from any active bid packets | Endorsement availability check |

| Vehicle use (owned / leased / hired) | Commercial auto need |

| CA contractor license number (if applicable) | CSLB compliance check |

| TX contractor license / DBA (if applicable) | TDI / city packet alignment |

Have most of this ready? Get a quote and we will turn it around quickly.

How fast can you get a contractor GL policy and a COI?

In brief: A clean quote packet often gets bound coverage within 1 to 3 business days, with COIs and Additional Insured endorsements available the same day after binding for most carriers.

Speed is usually about documentation, not the carrier. With a complete packet, a quote can come back the same or next business day, binding often happens within 1 to 3 business days, and a Certificate of Insurance can typically be issued the same day after binding. Common endorsements like Additional Insured, Primary & Noncontributory, and Waiver of Subrogation are added at or just after binding, and we can upload COIs to vendor portals and compliance platforms on your behalf. Already a client and just need paper? Request a COI.

Frequently asked questions about contractor general liability

What is general liability insurance for contractors and what does it cover?

General liability insurance for contractors is a third-party policy that covers bodily injury, property damage, and personal and advertising injury claims tied to your operations, plus the legal defense costs that come with them. If a visitor is hurt on your jobsite, or your crew damages a client's property, or a claim surfaces after a job is finished, GL responds. It does not cover your own employees, your own tools, your own vehicles, or your own faulty workmanship, which is why most contractors carry GL alongside workers' compensation and commercial auto.

Is general liability insurance legally required for contractors in California or Texas?

In most cases it is not a blanket state-law mandate. California's CSLB focuses on workers' compensation for licensees and proof of insurance in many bidding contexts, and Texas has no statewide board requiring GL for every contractor. In practice, though, GL is effectively required because contracts, leases, general contractors, vendor portals, and city permit packets ask for it before work begins. The honest way to say it: the law rarely forces GL on you, but the people who hire you almost always do.

How much does general liability insurance cost for a small contractor?

Most small contractors pay $75 to $300 per month for a standard $1M/$2M general liability policy, with light trades and handymen near the lower end and higher-hazard work near the top. A general contractor typically runs $150 to $400 per month, and roofing or other high-hazard work often runs $250 to $700 or more. Final pricing depends on underwriting and on your trade, revenue, payroll, claims history, and the limits your contracts require. The fastest way to get a real number is to send a complete quote packet.

What is the difference between a Certificate of Insurance and an Additional Insured endorsement?

A Certificate of Insurance (COI) is proof that a policy exists. It lists your coverages, limits, and dates, and it is what you hand a GC or vendor portal to show you are insured. An Additional Insured endorsement actually changes the policy, extending certain coverage to another party, such as a general contractor or property owner, for liability arising out of your work. A COI may name an Additional Insured, but the endorsement is what gives that party real rights under the policy. Many contracts require both.

Does general liability cover injuries to my employees or subcontractors?

No. Injuries to your own employees are handled by workers' compensation, not general liability. GL is a third-party policy, so it responds to people who are not your workers, such as a client, a visitor, or a delivery driver. Subcontractors are more nuanced: a properly insured sub should carry their own GL and workers' compensation, and you should collect their COIs. If a sub is uninsured, their exposure can effectively fall back to you and your carrier, which is why subcontractor documentation affects both your coverage and your premium.

Does general liability cover damage I cause to my own work or tools?

Generally no. GL is built around damage to other people's property and injury to third parties, not damage to your own work product or your own equipment. Faulty workmanship to the project itself is usually excluded or limited, tools and equipment are covered by an inland marine or tools-and-equipment policy, and property still under construction is covered by builder's risk. GL can respond when your faulty work causes resulting damage to other property, but the core idea is that GL protects others from your operations, not your own assets.

What are Additional Insured, Primary and Noncontributory, and Waiver of Subrogation?

These are three endorsements contracts commonly require together. Additional Insured extends certain coverage to another party, like a GC or owner, for liability arising out of your work. Primary and Noncontributory means your policy pays first and does not ask the other party's insurer to share. Waiver of Subrogation gives up your insurer's right to recover from that party after a claim. Together they shift risk toward your policy, which is exactly why GCs and project owners ask for them, and why they can affect your premium.

Can a contractor get a Certificate of Insurance the same day?

Often yes, once coverage is bound. If you already have an active policy, a standard COI can usually be issued the same day, and many Additional Insured endorsements can be added quickly as well. If you are starting from scratch, the timeline depends on getting a complete quote packet in, binding the policy, and then issuing the certificate, which together commonly takes 1 to 3 business days. We can also upload COIs directly to vendor portals and compliance platforms so you are not chasing paperwork before a job starts.

How does subcontractor usage affect my contractor general liability cost?

Subcontractor usage is one of the bigger levers in contractor GL pricing. Carriers want to know what percentage of your revenue goes to subs and how well you vet them. If your subs carry their own GL and workers' compensation and you collect their COIs, your risk transfer is clean and your rate reflects that. If subs are uninsured or undocumented, their exposure can be rated as yours, which raises your premium and can create coverage gaps. Strong subcontractor documentation is one of the most effective ways to keep your cost down.

What information do you need to give a contractor a GL quote?

To quote accurately we need your legal business name and DBA, your trade and detailed scope of work, your business address and where you work, your last and projected annual revenue, payroll with employee count and W-2 versus 1099 split, your subcontractor percentage and vetting process, five years of claims history or loss runs, the limits your contracts require, and any COI or endorsement wording from active bid packets. Vehicle use and your CA or TX contractor license number help too. A complete packet often turns into a same-day or next-business-day quote.

Ready to get contractor general liability coverage?

In brief: Send a quote packet and you will have a number to share with your GC, owner, or vendor portal in 1 to 3 business days, with COIs and endorsements available right after binding.

ContractorsInsured.net is an independent insurance brokerage built for contractors in California and Texas. We place general liability with multiple carriers, match the limits and endorsements your contracts require, and handle COIs and compliance uploads so you can keep working. This page was written and reviewed by Pascal Burke, Licensed Insurance Broker, CA License #6015321 and TX License #3305690. Learn more about us and read our disclosures.

This is general information, not legal advice. Coverage, eligibility, policy forms, endorsements, and pricing vary by carrier and underwriting approval. Specific contract language and bid packet requirements should be reviewed with your broker before binding.