How Much Does General Liability Insurance Cost in Stockton, California? 2026 Guide

Last updated: June 2026

Reviewed by: Pascal Burke, Licensed Insurance Broker

CA License #6015321

TX License #3305690

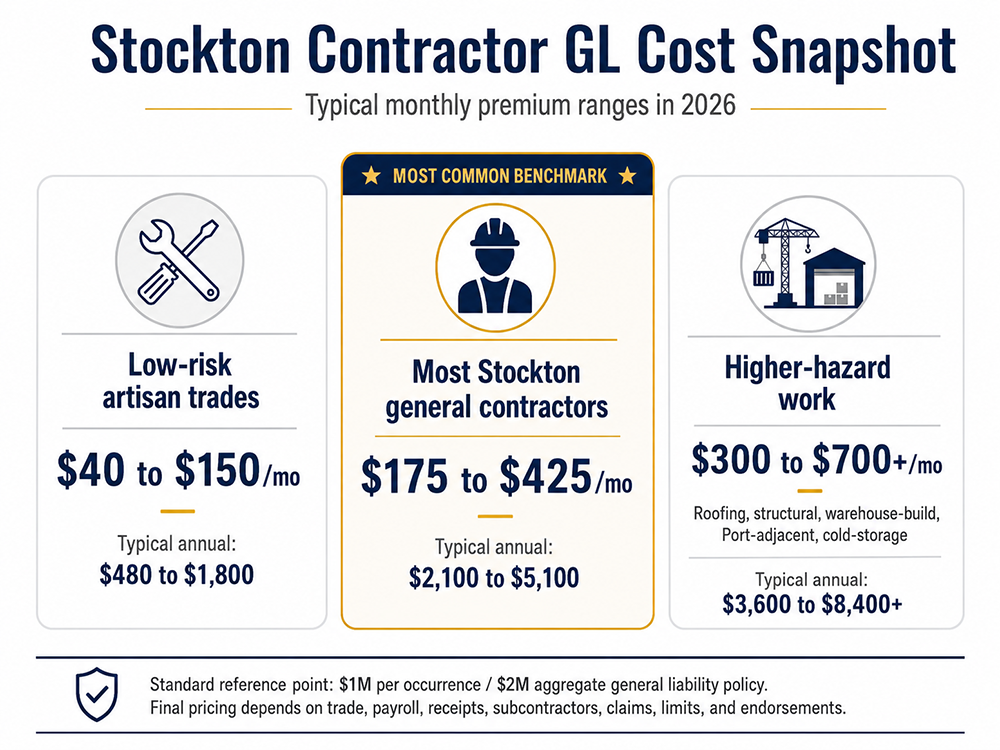

Most Stockton general contractors typically pay $175 to $425 per month ($2,100 to $5,100 per year) for a standard $1M per occurrence / $2M aggregate general liability policy, with roofers, structural trades, warehouse-build, Port-adjacent contractors, and contractors on cold-storage or food-processing projects often paying more. Stockton is usually less expensive than coastal California, but the city’s Port, logistics, warehouse, ag-processing, and public works exposure can push some contractors above a simple Central Valley average. The right premium depends on trade class, payroll, gross receipts, subcontractor usage, loss history, required endorsements, and whether the job requires fast COIs for a Port, warehouse, city, county, or vendor portal. As ContractorsInsured.net (CA Lic #6015321), we shop multiple California-admitted carriers for Stockton contractors, quote the same business day, and issue the COI right after binding.

What general liability insurance covers

In brief: General liability covers third-party bodily injury, third-party property damage, and personal and advertising injury, but it does not replace workers’ comp, auto, tools, bonds, professional liability, or builder’s risk.

General liability insurance is a third-party liability policy that responds to claims arising from a business’s operations, including bodily injury to non-employees, property damage to third parties, and personal and advertising injury. For contractors, it is the most commonly required coverage in contracts, leases, vendor portals, and city permit packets.

For Stockton contractors, what general liability covers matters because the certificate is often reviewed before the job starts. Warehouse operators, Port-related vendors, property managers, residential owners, and public agencies may all ask for proof that your policy can respond to claims arising from your work. The Insurance Information Institute describes Commercial General Liability as protection against financial loss for bodily injury, property damage, or personal and advertising injury caused by services, operations, or employees, up to policy terms and limits.

Scenario card 1: Port-adjacent warehouse trip and fall

A delivery driver walks through a Stockton Port-adjacent warehouse jobsite and trips over temporary materials staged by a contractor. The driver breaks an ankle and files a claim for medical costs and lost income. General liability can respond to third-party bodily injury allegations and pay defense costs if the contractor is sued.

Scenario card 2: Lodi remodel property damage

A plumbing crew working on a Lodi kitchen remodel cracks the homeowner’s tile floor while moving equipment. The owner claims the contractor caused damage to property outside the plumbing work. General liability can respond to third-party property damage, subject to exclusions and policy terms.

Scenario card 3: Tracy advertising injury allegation

A Tracy subcontractor uses a copyrighted jobsite photo in a social post to promote completed work. The photo owner sends a demand letter alleging unauthorized use. General liability may include personal and advertising injury coverage for certain covered allegations, depending on facts and policy wording.

Scenario card 4: Manteca completed operations claim

A Manteca roofing crew finishes a project. Six months later, a leak causes interior water damage. General liability may respond to resulting third-party property damage from completed operations, but it usually does not pay to redo the defective roof work itself.

Scenario card 5: Lathrop warehouse subcontractor lawsuit

A Lathrop warehouse general contractor is named in a lawsuit over a subcontractor’s installation work. Even when the GC did not personally perform the disputed task, general liability may pay defense costs if the claim falls within the policy and the GC is legally pulled into the dispute.

How much does general liability insurance cost in Stockton?

In brief: Most Stockton GCs land in the $175 to $425 monthly range, while lower-risk trades can be below that and higher-hazard Port, warehouse, roofing, and structural work can exceed it.

Most Stockton general contractors typically pay $175 to $425 per month, or $2,100 to $5,100 per year, for a standard $1M per occurrence / $2M aggregate general liability policy.

That range assumes a small to mid-sized contractor with ordinary residential, light commercial, remodel, repair, or tenant-improvement work. It does not assume major structural work, high payroll, frequent subcontractor usage, large warehouse builds, cold-storage projects, Port-adjacent vendor requirements, or repeated losses.

Stockton contractor profile | Typical monthly GL cost | Typical annual GL cost | Notes |

|---|---|---|---|

Low-risk artisan or small service trade | $40 to $150 | $480 to $1,800 | Often small payroll, fewer subcontractors, lower contract limits |

Typical Stockton general contractor | $175 to $425 | $2,100 to $5,100 | Common range for $1M/$2M coverage |

Roofing, structural, warehouse-build, Port-adjacent, cold-storage, or food-processing work | $300 to $700+ | $3,600 to $8,400+ | Higher hazard class, contract requirements, and completed-operations exposure |

Larger GC with multiple crews or heavy subcontractor usage | $500 to $1,200+ | $6,000 to $14,400+ | Premium depends heavily on receipts, payroll, certificates, and loss history |

Contractor needing umbrella or excess for larger contracts | Varies | Varies | Often added when contracts require $5M or more total liability limit |

Unlike national aggregator averages, this guide is written around Stockton contractor risks, including Port of Stockton vendor requirements, I-5 and Highway 99 warehouse corridors, San Joaquin County job sites, cold-storage work, and public works insurance packets.

If you are comparing Stockton to nearby Central Valley markets, review our guides to general liability insurance cost in Fresno and general liability insurance cost in Sacramento. The pricing logic is similar, but Stockton’s Port, warehouse, and logistics mix can change underwriting.

Why contractor GL pricing reflects Stockton’s logistics + warehouse mix

In brief: Stockton is not priced like a coastal downtown market, but Port, logistics, warehouse, ag-processing, and cold-storage jobs can raise the carrier’s view of severity.

Stockton’s insurance profile is a Central Valley profile with a logistics overlay. A residential remodeler working in north Stockton, Lodi, Manteca, or Ripon may price closer to a lower-cost inland market. A contractor working around the Port of Stockton, large warehouses in Lathrop or Tracy, food-processing facilities, cold-storage buildings, rail-served properties, or commercial distribution sites may face a higher underwriting load.

The Port’s official business materials describe Stockton as an inland deepwater port with dry and liquid bulk cargo, warehouse storage, road access, and rail access. That matters because insurers do not only price the city. They price what could go wrong on the jobsite.

“In 15+ years writing California contractor GL, the #1 reason Stockton Port and logistics warehouse COIs get rejected is not the policy, it is missing the operator’s exact Additional Insured + Primary Noncontributory wording. Read the schedule before you bind.”

Pascal Burke, Licensed Insurance Broker (CA #6015321, TX #3305690)

A warehouse GC may need broader Additional Insured wording, completed-operations protection, Primary and Noncontributory language, Waiver of Subrogation, higher limits, and proof that subcontractors carry their own coverage. A contractor working near forklifts, docks, trucks, racking, cold-storage equipment, concrete tilt-up work, roof penetrations, or food-processing machinery creates a different severity profile than a small interior repair contractor.

That is why general liability insurance for California contractors should be quoted around the exact scope of work, not just the ZIP code.

Cost by coverage limit

In brief: $1M/$2M is the common small-contractor baseline, but Port, warehouse, public works, and larger commercial contracts may require $2M/$4M or excess limits.

A Stockton contractor can often start with $1M per occurrence / $2M aggregate general liability, but larger warehouse, Port, logistics, and public works contracts may require $2M/$4M or a total liability tower of $5M or more.

Coverage structure | Typical Stockton use case | Premium impact | Notes |

|---|---|---|---|

$1M per occurrence / $2M aggregate | Common baseline for many residential and light commercial contractors | Baseline | Often enough for smaller private jobs, leases, and vendor packets |

$2M per occurrence / $4M aggregate | Larger warehouse, logistics, property manager, or public contract requirement | Moderate increase | Some carriers offer this by endorsement, others require different underwriting |

$1M/$2M plus $1M umbrella | Contract wants higher total protection but not a full $5M tower | Moderate to significant increase | Depends on trade, auto exposure, payroll, and claims |

$1M/$2M plus $4M umbrella | Port, larger warehouse, institutional, or enterprise vendor requirement | Significant increase | Underwriter reviews loss history, safety controls, subcontractor certificates, and operations |

Project-specific higher limits | One large project or vendor portal requirement | Case by case | May require contract review before binding |

The right limit depends on the contract. A small residential client may only ask for a COI. A warehouse operator may ask for specific endorsement forms. A public agency may require the City, its officers, officials, employees, and volunteers to be named as additional insureds, as shown in City of Stockton insurance requirement exhibits.

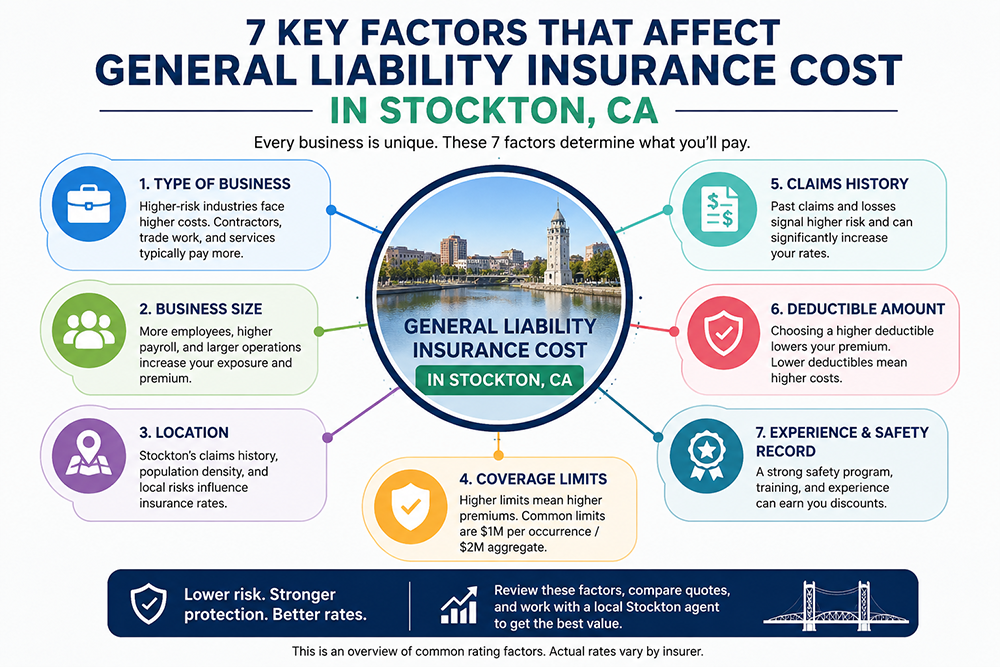

The 7 factors carriers use to price your policy

In brief: Trade class, receipts, payroll, subcontractors, claims, limits, and contract wording usually explain most premium differences between two Stockton contractors.

Stockton contractor GL premiums move up or down based on the risk the carrier expects to insure, the contract language the policy must satisfy, and the severity of the jobsite exposure.

Cost factor | Why it matters in Stockton | Premium direction |

|---|---|---|

Trade classification | Roofing, structural, concrete, demolition, framing, and exterior work usually rate higher than low-risk interior trades | Higher hazard means higher premium |

Gross receipts | Carriers often rate GL partly on annual revenue because receipts reflect job volume | More revenue usually increases premium |

Payroll | Payroll signals crew size and operational scale | Larger payroll can increase premium |

Subcontractor usage | Heavy subcontracting increases certificate tracking and completed-operations risk | Missing subcontractor COIs can raise cost or block coverage |

Claims history | Prior trip-and-fall, water damage, completed operations, or property damage claims affect underwriting | Clean history improves carrier options |

Coverage limits and endorsements | Higher limits, Additional Insured, Primary and Noncontributory, and Waiver of Subrogation can affect eligibility and pricing | More requirements can increase cost |

Jobsite type | Port, warehouse, cold-storage, food-processing, and public works settings can raise severity | Higher-complexity sites cost more |

Carriers also look at whether you maintain written subcontractor agreements, safety practices, certificates from subs, and clear scopes of work. OSHA describes construction as a high-hazard industry involving construction, alteration, and repair work, with hazards such as falls, struck-by incidents, electrocutions, silica dust, and asbestos exposure. Strong jobsite controls can help your submission look cleaner.

For a deeper explanation of GL cost factors and limits, compare your operations against the rating factors above before requesting quotes.

Stockton contract, lease, and COI requirements

In brief: Many Stockton contracts are less about buying a policy and more about delivering the exact COI, endorsement, and contract wording before work begins.

Stockton contractors often need general liability because a contract, lease, vendor portal, property manager, public agency, warehouse operator, or general contractor requires it. California law does not create one universal general liability requirement for every contractor, but contracts often do.

Common Stockton COI requirements include:

Requirement | Where Stockton contractors see it | Why it matters |

|---|---|---|

Certificate of Insurance | Property managers, GCs, Port vendors, warehouse operators, city or county contracts | Shows active coverage and limits |

Additional Insured wording | Public agencies, warehouse owners, Port-related contracts, GCs | Extends insured status to the requesting party for covered operations |

Primary and Noncontributory wording | City, Port, warehouse, institutional, and enterprise contracts | Says your policy responds before the requesting party’s insurance |

Waiver of Subrogation | Public works, warehouse contracts, some GC agreements | Limits the insurer’s recovery rights against the party requiring the waiver |

Completed operations language | Roofing, exterior, structural, tenant improvement, warehouse, and GC contracts | Helps address claims arising after the work is finished |

Subcontractor certificate tracking | GCs and larger project owners | Reduces uncovered subcontractor risk |

Higher limits or umbrella | Port, logistics, public works, and larger commercial projects | Required when contract limits exceed standard $1M/$2M |

Start with Certificate of Insurance basics before you bid a Stockton job that requires proof of coverage. Then confirm whether the contract asks for an Additional Insured endorsement and a Waiver of Subrogation.

The Port of Stockton’s standard insurance language requires service providers to furnish certificates and amendatory endorsements, maintain insurance with acceptable insurers, and ensure subcontractors maintain insurance meeting the stated requirements. The City of Stockton’s contract insurance exhibits similarly include Additional Insured status, Primary and Noncontributory wording, and Waiver of Subrogation provisions.

DIR also requires public works contractors to register, pay prevailing wages, follow apprenticeship requirements, and maintain certified payroll records. Those rules are separate from GL, but they often appear in the same public works compliance package.

What general liability does NOT cover

In brief: GL protects against many third-party claims, but it is not a substitute for workers’ comp, commercial auto, tools coverage, bonds, E&O, or builder’s risk.

General liability is foundational, but it is not an all-risk policy. Stockton contractors should know the common gaps before relying on a COI to satisfy a job requirement.

Exposure | Usually not covered by GL | Coverage to review |

|---|---|---|

Employee injuries | Workers hurt on the job | Workers’ compensation |

Business vehicles | Owned, hired, or non-owned vehicle accidents | Commercial auto |

Your tools and equipment | Theft, fire, or damage to your own tools | Inland marine |

Contract performance | Failure to complete work or meet bond terms | Contractor bond |

Professional design errors | Design, consulting, engineering, or spec mistakes | Professional liability or E&O |

Damage to your own defective work | Rework, faulty workmanship, or replacing your own work | Warranty, workmanship, or project-specific coverage review |

Course of construction property | Damage to a building under construction | Builder’s risk |

Pollution, mold, asbestos, or lead | Environmental or hazardous material claims | Pollution liability or specialty coverage |

California contractors with employees must carry workers’ compensation coverage, and CSLB explains that employers in construction must carry it even if they have only one employee. Certain license classifications also cannot claim a workers’ compensation exemption under CSLB rules.

If you are one of the general contractors managing subs, job schedules, materials, and owner contracts, the GL gap analysis should be part of your bid review.

How Stockton contractors can lower GL costs without creating coverage gaps

In brief: The best savings usually come from better documentation, clean subcontractor controls, safer jobsites, accurate class codes, and quoting before a deadline.

The cheapest policy is not always the best policy. A low premium can become expensive if the COI gets rejected, the endorsement wording is wrong, or the policy excludes work you actually perform.

Practical ways to reduce GL cost without creating coverage gaps include:

Classify your work accurately. Do not quote as a handyman if you perform roofing, structural, or GC work.

Keep subcontractor COIs current. Require every subcontractor to provide active GL and workers’ comp where required.

Use written subcontractor agreements. Written risk transfer can improve underwriting and reduce claim disputes.

Document jobsite safety. Safety plans, toolbox talks, fall protection, housekeeping, and equipment controls help tell a better risk story.

Review Port and warehouse packets before binding. Extra endorsements can change eligibility, premium, and turnaround time.

Avoid last-minute COI requests. Same-day certificates are possible, but same-day contract review is harder.

Disclose prior claims clearly. A clean explanation is better than an underwriter discovering missing information.

Ask about higher deductible or retention options only when appropriate. Saving premium is not useful if the retention strains cash flow.

Bundle policies only when the coverage fit is correct. Package pricing can help, but not if it leaves tools, auto, or WC exposed.

Use a contractor-focused broker. Contractor submissions need trade, contract, and endorsement fluency.

SBA explains that general liability can protect a business against financial loss from bodily injury, property damage, medical expenses, libel, slander, defending lawsuits, settlements, and judgments. That is why the goal is not simply to cut premium. The goal is to keep protection strong while removing avoidable underwriting friction.

What to prepare before requesting a quote

In brief: A fast Stockton GL quote depends on accurate operations, receipts, payroll, license details, subcontractor use, claims history, and contract wording.

A Stockton contractor can often speed up quote turnaround by providing the right information before the broker submits to carriers.

Quote item | What to provide | Why it matters |

|---|---|---|

Legal business name | Entity name, DBA, mailing address, and jobsite area | Needed for application and policy issuance |

CSLB license number | Active license number and classification | Confirms trade and license status |

Description of operations | Exact work performed and excluded work | Prevents wrong class code and policy mismatch |

Annual gross receipts | Last year and projected next 12 months | Core rating input |

Annual payroll | Owner, employee, and crew payroll | Helps underwriter size operations |

Subcontractor cost | Annual subcontracted work and certificate process | Heavy sub use changes risk |

Prior claims | Date, type, amount paid, and status | Required for underwriting |

Current policy | Declarations page if insured now | Helps compare limits and gaps |

Contract sample | Port, warehouse, GC, city, county, or vendor portal requirements | Needed to confirm endorsements before binding |

Port of Stockton / warehouse vendor portal? | Yes or no, plus exact portal language | Determines COI and endorsement needs |

Requested limits | $1M/$2M, $2M/$4M, umbrella, or project-specific | Affects quote strategy |

Desired COI deadline | When proof is needed | Controls urgency and carrier selection |

“Before you ask for the lowest Stockton GL premium, send the broker the contract page that lists insurance requirements. A $200 cheaper policy is not cheaper if it cannot issue the Additional Insured, Primary Noncontributory, or Waiver wording your customer requires.”

Pascal Burke, Licensed Insurance Broker (CA #6015321, TX #3305690)

For broader state context, review California contractor GL requirements before requesting a quote. If you need a same-day certificate on an active policy, existing clients can Request a COI.