What general liability insurance covers

In brief: General liability helps Sacramento contractors pay for covered third-party injury, third-party property damage, advertising injury, completed operations claims, and defense costs.

General liability insurance is a third-party liability policy that responds to claims arising from a business’s operations, including bodily injury to non-employees, property damage to third parties, and personal and advertising injury. For contractors, it is the most commonly required coverage in contracts, leases, vendor portals, and city permit packets.

For Sacramento contractors, this coverage matters because job sites often involve owners, tenants, delivery drivers, inspectors, agency representatives, other trades, and the public. A basic policy for general liability insurance for contractors normally includes premises and operations coverage, products and completed operations coverage, personal and advertising injury coverage, and legal defense for covered claims.

Scenario 1: State-facility jobsite injury

A delivery driver brings materials to a Sacramento state-facility jobsite, trips over stored conduit near the access path, and breaks an ankle. If the contractor is accused of creating an unsafe third-party condition, GL can respond to covered injury and defense costs.

Scenario 2: Elk Grove remodel property damage

A plumbing crew working on an Elk Grove remodel cracks the homeowner’s tile floor while moving equipment through a finished hallway. GL can help pay for covered third-party property damage caused during operations, subject to policy terms and exclusions.

Scenario 3: Roseville advertising injury

A Roseville subcontractor uses a copyrighted jobsite photo in a social media post without permission. Personal and advertising injury coverage may respond if the allegation fits the policy language and no exclusion applies.

Scenario 4: Folsom completed operations leak

A Folsom roofing crew finishes a project. Six months later, a leak causes interior water damage. Completed operations coverage may respond to resulting third-party property damage, while the cost to redo the contractor’s own faulty work may still be excluded.

Scenario 5: Rancho Cordova defense costs

A Rancho Cordova general contractor is named in a lawsuit over a subcontractor’s work. Even if the GC believes the subcontractor caused the problem, GL may help pay defense costs when the lawsuit alleges covered bodily injury or property damage.

For the policy foundation behind these examples, see what general liability covers.

How much does general liability insurance cost in Sacramento?

In brief: Most Sacramento GCs land around $200 to $500 per month for $1M/$2M GL, but roofers, structural trades, high payroll contractors, and public works contractors often pay more.

Most Sacramento general contractors typically pay $200 to $500 per month, or $2,400 to $6,000 per year, for a standard $1M per occurrence / $2M aggregate general liability policy.

That range assumes a contractor with clean or manageable claims history, standard operations, accurate class codes, and a normal mix of residential or middle-market commercial work. Sacramento can price slightly above a generic California middle-market average because public contracts, prevailing wage work, subcontractor certificates, and agency-specific endorsements often add underwriting scrutiny.

Unlike national aggregators that quote $40 to $150 per month for a generic small business, this Sacramento contractor guide prices GL around trade class, payroll, subcontractor exposure, public contract endorsements, and $1M/$2M or higher limits.

| Sacramento contractor profile | Typical monthly GL estimate | Typical annual GL estimate | Why the range moves |

|---|---|---|---|

| Handyman or light residential trade with low revenue | $75 to $200 | $900 to $2,400 | Lower job severity, smaller payroll, fewer subcontractors |

| Standard Sacramento general contractor | $200 to $500 | $2,400 to $6,000 | Broader operations, owner contracts, COI requests |

| Roofing, structural, excavation, or high-hazard trade | $300 to $700+ | $3,600 to $8,400+ | Higher claim severity and completed operations exposure |

| State agency or public works contractor | $300 to $700+ | $3,600 to $8,400+ | Higher payroll base, endorsement review, stricter contract language |

| Contractor with prior GL claims or poor documentation | Varies widely | Varies widely | Loss history and incomplete subcontractor controls can narrow markets |

| Trade or operation in Sacramento | Common GL cost pattern | Underwriting concern |

|---|---|---|

| General contractor | $200 to $500 per month | Subcontractor controls, completed operations, contract requirements |

| Plumbing contractor | $150 to $450 per month | Water damage, finished interior work, service calls |

| Electrical contractor | $150 to $400 per month | Fire risk, service work, commercial exposure |

| Roofing contractor | $300 to $700+ per month | Height exposure, completed operations, water intrusion |

| Concrete or structural trade | $250 to $650+ per month | Structural failure, heavy jobsite equipment, public works projects |

| Finish carpentry or painting | $100 to $350 per month | Lower severity, but depends on commercial work and payroll |

For statewide context, compare this with general liability insurance for California contractors. For a coastal metro comparison, see general liability insurance cost in Los Angeles and general liability insurance cost in San Diego.

Get a Quote

Why contractor GL pricing reflects state-capital construction

In brief: Sacramento GL pricing reflects the mix of state agency work, prevailing wage payroll, public works exposure, commercial infill, suburban growth, and California contract compliance.

Sacramento is not priced only like a suburban residential market. It is the California state capital, with a steady ecosystem of agency, school, municipal, healthcare, infrastructure, and public-facility work. Contractors bidding jobs connected to DGS, Caltrans, CDCR, DSA, community colleges, K-12 schools, state-leased space, or Sacramento municipal facilities may face more detailed insurance instructions than a small private remodel.

The premium effect often starts with payroll and revenue. DIR states that public works generally includes construction, alteration, demolition, installation, or repair paid in whole or in part with public funds, and that workers on public works projects must be paid prevailing wages. Higher payroll can increase the exposure base for GL rating, especially where carriers rate by payroll, revenue, or subcontractor cost. The California Department of Insurance also notes that general liability premiums may be developed from exposure bases such as square footage, payroll, or gross sales, depending on classification.

“Sacramento contractors bidding state agency or public works projects should treat the insurance schedule as part of the bid, not an afterthought. Prevailing wage payroll, subcontractor certificates, and exact endorsement wording can change both price and carrier appetite before a COI is ever issued.”

Pascal Burke, Licensed Insurance Broker (CA #6015321, TX #3305690)

Sacramento also has mixed project density. Midtown, Downtown, K Street, Land Park, Natomas, and Pocket-Greenhaven can involve tight access, pedestrian exposure, tenants, deliveries, and neighboring property. Elk Grove, Folsom, Roseville, Rancho Cordova, Citrus Heights, Carmichael, Davis, West Sacramento, and Arden-Arcade add a different mix of residential growth, commercial buildouts, service work, and subcontracted projects.

This is why a Sacramento contractor should not rely on a generic statewide quote. A carrier wants to know what work you perform, where you perform it, who your customers are, whether you subcontract, what contracts require, and whether your certificates need special wording.

Cost by coverage limit

In brief: $1M/$2M is the common baseline, $2M/$4M is often requested for larger contracts, and umbrella or excess liability may be needed for $5M+ requirements.

Most Sacramento contractor GL quotes start with $1,000,000 per occurrence and $2,000,000 aggregate. That is the common baseline for private contracts, landlords, many GCs, and vendor portals. Larger commercial, municipal, or state-agency work may require higher limits or an umbrella layer.

| Coverage limit requested | Typical Sacramento use case | Monthly pricing effect | Notes |

|---|---|---|---|

| $1M per occurrence / $2M aggregate | Standard private jobs, many GC requirements, leases | Baseline | Most common starting point |

| $2M per occurrence / $4M aggregate | Larger commercial jobs, some public or institutional contracts | Moderate increase | Carrier may endorse higher aggregate or quote higher base limits |

| $1M/$2M plus $1M umbrella | Contracts asking for extra protection above GL | Added premium | Umbrella underwriting reviews auto, payroll, and operations |

| $1M/$2M plus $5M umbrella or excess | State agency, larger public works, infrastructure, institutional work | Significant increase | Often requires full submission and contract review |

| Project-specific requirement | Unique agency or owner contract | Varies | Exact wording can affect market selection |

For a deeper policy explanation, review general liability cost factors and limits before selecting limits only by price.

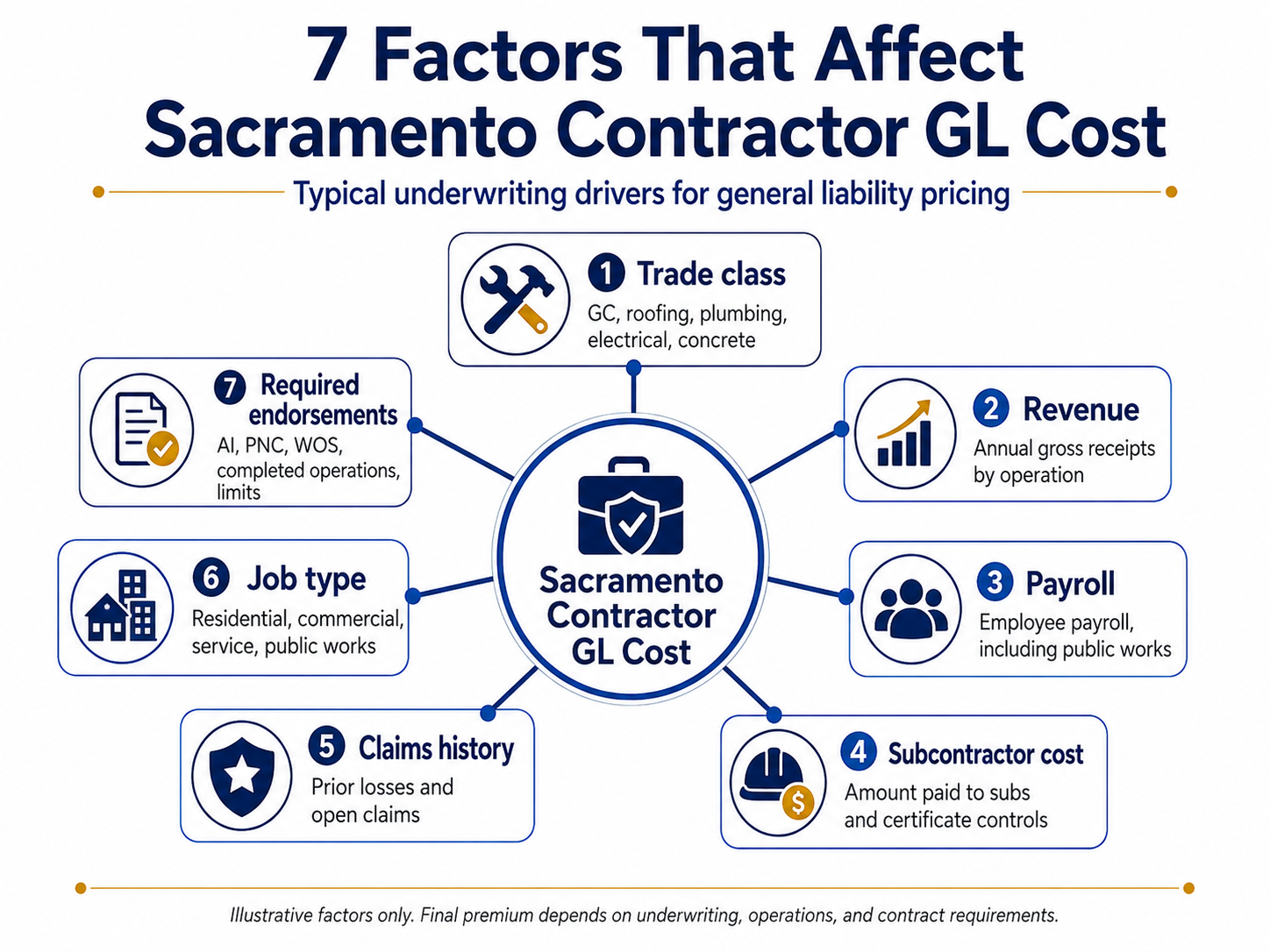

The 7 factors carriers use to price your policy

In brief: Carriers price Sacramento contractor GL by class code, revenue, payroll, subcontractor cost, job type, claims history, and requested endorsements.

Every carrier has its own rating model, but most contractor GL submissions are built around the same core underwriting questions. Sacramento adds an extra layer because public works, state agency contracts, school work, airport-related projects, and municipal work often require tighter paperwork.

| Pricing factor | What the carrier reviews | Sacramento example | Premium impact |

|---|---|---|---|

| 1. Trade classification | Exact work performed | GC, roofer, plumber, electrician, concrete contractor | High |

| 2. Annual revenue | Gross receipts by operation | Residential remodel revenue vs commercial tenant improvements | High |

| 3. Payroll | Employee payroll by trade | Prevailing wage payroll on public works jobs | High |

| 4. Subcontractor cost | Amount paid to subs and certificate controls | GC using framing, roofing, plumbing, and electrical subs | High |

| 5. Job type | Residential, commercial, public, industrial, service work | DGS facility work vs Elk Grove remodels | Medium to high |

| 6. Claims history | Prior GL losses and open claims | Water intrusion, trip and fall, property damage | High |

| 7. Contract wording | AI, PNC, WOS, completed operations, primary wording | State agency or municipal certificate instructions | Medium to high |

The most common avoidable problem is mismatch. If the application says residential remodeling but the contract shows state-facility structural work, the quote may change, get delayed, or be declined.

Sacramento contract, lease, and COI requirements

In brief: Sacramento contracts often require proof of GL through a COI, plus endorsements such as Additional Insured, Primary and Noncontributory, and Waiver of Subrogation.

A Certificate of Insurance is not the policy itself. It is a summary document showing the insurance carried by the contractor at the time the certificate is issued. For a Sacramento contractor, COIs may be requested by general contractors, property managers, state agencies, school districts, municipal departments, landlords, lenders, and vendor platforms.

The California Department of General Services publishes contractor insurance guidance for vendors doing business with DGS, and state or local contract packets may require proof of coverage before work begins. Read the insurance schedule carefully before binding coverage, especially if the contract asks for specific additional insured wording, completed operations status, primary and noncontributory language, waiver language, or higher limits.

Common Sacramento COI requests include:

- The certificate holder name and address exactly as written in the contract.

- General liability limits, usually starting at $1M/$2M.

- The owner, agency, landlord, or GC named as additional insured.

- Primary and noncontributory wording where required.

- Waiver of Subrogation where required by contract.

- Completed operations status for a set period after the work.

- Separate auto, workers comp, umbrella, or builder’s risk evidence.

Before you submit a bid packet or mobilize to a jobsite, review Certificate of Insurance basics, the Additional Insured endorsement, and Waiver of Subrogation requirements.

Existing clients can also Request a COI.

What general liability does NOT cover

In brief: GL is essential, but it does not replace workers comp, commercial auto, tools coverage, professional liability, builder’s risk, or surety bonds.

General liability is broad, but it is not a catch-all contractor insurance policy. A Sacramento contractor who buys GL and stops there may still have major coverage gaps.

GL typically does not cover:

- Employee injuries, which are usually handled through workers compensation.

- Damage to your own tools, equipment, or materials.

- Auto accidents involving company vehicles or hired vehicles.

- Professional design errors, engineering errors, or consulting mistakes.

- Faulty workmanship itself, even when resulting damage may be considered separately.

- Contractual penalties, fines, or liquidated damages.

- Pollution claims unless endorsed.

- Employee wage claims, DIR penalties, or payroll compliance issues.

- Bond obligations.

- Property under construction when builder’s risk is required.

CSLB requires acceptable workers compensation documentation for contractors who must carry workers comp, and DIR contractor registration rules for public works also include workers compensation and CSLB license requirements where applicable. That is separate from GL.

For Sacramento general contractors, the common package is GL, workers comp, commercial auto, inland marine, umbrella or excess, and contract-specific endorsements. Public works, state agency jobs, and larger commercial projects may add bonds, builder’s risk, or professional liability depending on the scope.

How Sacramento contractors can lower GL costs without creating coverage gaps

In brief: The safest way to lower GL cost is to improve underwriting quality, not to understate operations, skip endorsements, or buy limits below contract requirements.

A cheaper policy is not always a better policy. Sacramento contractors can often improve pricing by giving carriers cleaner information and reducing avoidable risk signals.

Smart cost-control steps include:

- Use accurate class codes and describe your work clearly.

- Separate residential, commercial, service, and public works revenue.

- Keep updated COIs from every subcontractor.

- Require subcontractors to name you as additional insured when appropriate.

- Track payroll and subcontractor cost by job type.

- Provide a clean loss history or explain old claims.

- Review bid packets before requesting a quote.

- Avoid buying a policy that excludes your real operations.

- Ask whether a higher deductible, package policy, or umbrella structure is more efficient.

- Work with a broker who understands California contractor GL requirements.

Do not reduce premium by hiding roofing, structural work, excavation, condo work, school work, or subcontractor exposure. If the carrier later determines the business was misclassified, the contractor can face audit premium, denial risk, cancellation, or a certificate problem at the worst possible time.

What to prepare before requesting a quote

In brief: A Sacramento contractor quote moves faster when the broker has your license details, revenue, payroll, subcontractor costs, contracts, COI instructions, and loss history upfront.

A complete submission helps your broker quote the right carrier the first time. This matters in Sacramento because state-agency and public works bid packets often include endorsement wording that cannot be solved after the policy is bound.

“The fastest Sacramento GL quotes come from contractors who send the insurance page of the contract with the application. A two-minute review of AI, Waiver, completed operations, and limit wording can prevent a same-day quote from becoming a same-week correction.”

Pascal Burke, Licensed Insurance Broker (CA #6015321, TX #3305690)

| Quote item | What to provide | Why it matters |

|---|---|---|

| Legal business name | Exact entity name and DBA | Prevents certificate and policy mismatch |

| CSLB license number | Active license number and classifications | Confirms trade and California contractor status |

| Entity type | Sole proprietor, corporation, LLC, partnership | LLCs may trigger separate liability insurance rules |

| Annual revenue | Estimated next 12 months | Major rating exposure |

| Payroll | Estimated next 12 months by trade | Important for GL rating and public works context |

| Subcontractor cost | Annual amount paid to subs | Determines subcontractor exposure |

| Job mix | Residential, commercial, public works, service, remodel, new construction | Helps carrier match class and appetite |

| Prevailing-wage state contract? Y/N | Identify DGS, Caltrans, school, municipal, or other public work | Helps quote required limits and endorsements |

| COI instructions | Upload contract insurance page | Confirms AI, PNC, WOS, certificate holder, and limits |

| Prior claims | Loss runs or claim details | Explains risk and improves market access |

Get a Quote

Frequently asked questions about contractor general liability in Sacramento

In brief: These answers cover the most common Sacramento contractor GL cost, legal, public works, COI, and quote-preparation questions.