Editorial note: This article is educational and intended for contractors and the professionals who advise them. ContractorsInsured.net is a licensed insurance brokerage (CA License #6015321; TX License #3305690), not a law firm or claims adjuster. Premium audit outcomes generally depend on the specific carrier, audit findings, applicable rating bureau rules (WCIRB in California, NCCI in most other states), and the contractor’s records. Always confirm specific audit responses with your broker, the auditor, and qualified counsel or your CPA before disputing or paying an audit bill.

“Most Dallas contractors don’t lose jobs because their general liability premium was too high; they lose jobs because the policy doesn’t match the contract wording. Get the COI requirements and additional insured language right before you bind, and the price almost always takes care of itself.”

Pascal Burke, Licensed Insurance Broker (CA #6015321 / TX #3305690), Founder of ContractorsInsured.net

Dallas, TX general liability insurance at a glance for 2026

Commercial General Liability (CGL) insurance for Dallas, TX contractors is a small business policy that covers third-party bodily injury, property damage, and personal/advertising injury claims arising from your business operations or completed work. As of 2026, most Dallas contractors should expect to pay $150 to $400+ per month for a $1M/$2M CGL policy, while lower-risk small businesses often pay $40 to $150 per month. Most contractors searching for a general liability insurance quote Dallas or comparing cheap general liability insurance Dallas contractors options are trying to understand what coverage will cost before signing a lease, submitting a bid, starting a job, or sending proof of insurance to a GC, landlord, vendor portal, or project owner. Final premium depends on trade, revenue, payroll, subcontractor usage, claims history, coverage limits, and required endorsements. Contractors looking for small business general liability Dallas coverage or a 1 million general liability insurance cost estimate should still get a personalized quote. As ContractorsInsured.net (TX Lic #3305690), we shop multiple Texas-admitted carriers for Dallas contractors, quote the same business day, and issue the COI right after binding.

Trade-specific guides: general liability for general contractors in Dallas · general liability for roofers in Dallas · general liability for plumbers in Dallas

These are Dallas figures. For nationwide context, see our national general liability insurance cost benchmarks.

Quick answer / TLDR

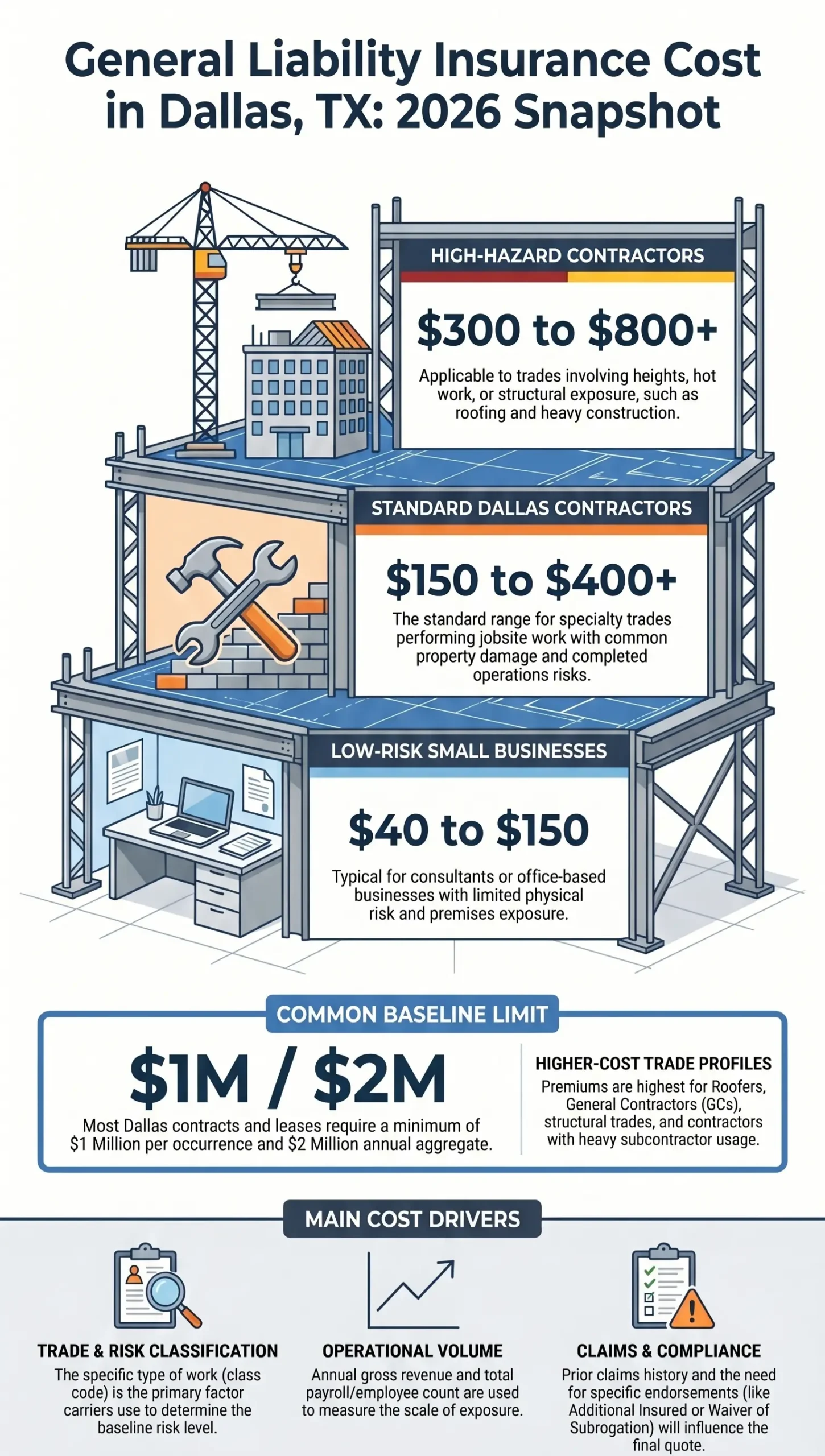

As of 2026, general liability insurance in Dallas, TX costs $40 to $150 per month for most small businesses and $150 to $400+ per month for contractors, on a standard $1 million per occurrence / $2 million aggregate policy.

Larger GCs, roofers, subcontractor-heavy operations, structural trades, high-revenue contractors, and businesses with prior claims may pay more. Dallas contracts, leases, GCs, vendor portals, and municipal requirements may also ask for a Certificate of Insurance, additional insured wording, waiver of subrogation, business auto, workers’ comp, or higher limits. The fastest way to price coverage correctly is to send your trade, revenue, payroll, subcontractor details, claims history, and contract wording to a contractor-focused broker. Get a Quote

Key facts at a glance

- Typical small business range: $40 to $150 per month in Dallas, TX (2026).

- Typical contractor range: $150 to $400+ per month, depending on trade and risk.

- Common baseline policy: $1 million per occurrence / $2 million aggregate ($1M/$2M).

- Top cost factors: trade class, revenue, payroll, subcontractor usage, claims history, required limits and endorsements.

- Common contract requests: Certificate of Insurance, additional insured, primary and noncontributory, waiver of subrogation, completed operations.

- Highest-priced trades: roofing, structural, demolition, and subcontractor-heavy general contractors.

What general liability insurance covers

In brief: General liability insurance helps protect Dallas businesses and contractors against certain third-party injury, property damage, personal injury, advertising injury, and legal defense costs. It does not replace workers’ comp, commercial auto, tools coverage, or every contract-required endorsement. Commercial general liability, often called CGL or GL, is one of the first policies many contractors need because it helps respond to covered claims involving bodily injury, property damage, and personal or advertising injury. The Texas Department of Insurance commercial general liability explainer describes CGL as coverage that protects business owners against claims of liability for bodily injury, property damage, and personal and advertising injury, including premises and operations exposure. For Dallas contractors, GL is often tied to jobsite access and paperwork. A project owner, landlord, GC, public entity, property manager, or vendor portal may ask for proof of insurance before work begins. That proof is usually shown through a certificate of insurance. A contractor general liability policy may help with claims involving:

- Third-party bodily injury: A customer, visitor, tenant, or other non-employee alleges they were injured because of your work or business operations.

- Third-party property damage: Your work damages someone else’s home, building, materials, fixture, vehicle, or property.

- Products and completed operations: A claim appears after the work is finished, such as damage tied to completed installation, repair, remodeling, or construction work.

- Personal and advertising injury: Certain covered claims involving libel, slander, copyright issues in advertising, or related allegations.

- Legal defense costs: Attorney fees, settlements, or judgments may be covered when the claim falls within the policy terms.

For contractors, general liability insurance for contractors is not just a generic business policy. It can be the difference between being approved for a Dallas project and being blocked because your COI does not meet the contract requirements.

How much does general liability insurance cost in Dallas?

In brief: As of 2026, the typical general liability insurance cost in Dallas, TX depends on the business type and risk level. Lower-risk businesses may pay under $150 per month, while many contractors should budget closer to $150 to $400+ per month. The best answer for general liability insurance cost Dallas TX is a range, not a fixed price. Insurance carriers price GL based on underwriting details. A consultant, retail shop, plumber, roofer, electrician, and general contractor will not be priced the same way. Here is a practical 2026 cost range for Dallas businesses and contractors.

| Business Type | Estimated Monthly Range | Estimated Annual Range | Why It Prices That Way |

| Low-risk consultant or office business | $40 to $75 | $480 to $900 | Limited physical risk, lower premises exposure, fewer property damage claims |

| Retail or customer-facing business | $60 to $150 | $720 to $1,800 | Customer traffic, premises exposure, possible slip-and-fall claims |

| Restaurant or food service business | $90 to $250 | $1,080 to $3,000 | Customer traffic, vendor requirements, food service exposure, premises risk |

| Specialty contractor | $150 to $300+ | $1,800 to $3,600+ | Jobsite work, property damage risk, completed operations, COI requirements |

| General contractor | $200 to $450+ | $2,400 to $5,400+ | Subcontractor exposure, project oversight, contract wording, completed operations |

| Roofing or high-hazard contractor | $300 to $800+ | $3,600 to $9,600+ | Heights, tear-offs, hot work, structural exposure, higher claim severity potential |

These are planning ranges, not guaranteed premiums. Your final quote may be lower or higher depending on trade class, annual revenue, payroll, employee count, subcontractor usage, claims history, coverage limits, endorsements, job type, prior coverage, and carrier appetite. Dallas contractors working across Dallas County, Collin County, Denton County, Rockwall County, Irving, Garland, Richardson, Plano, Frisco, McKinney, Mesquite, and other North Texas job sites should expect underwriting to focus on the actual work performed, not just the city name. A finish trade with lower hazard exposure may be easier to place than a roofer, structural contractor, excavation contractor, or GC with heavy subcontractor usage. This Dallas guide is also separate from the Fort Worth general liability insurance cost guide. Dallas and Fort Worth are both part of North Texas, but the search intent, job market, client base, contract requirements, and local business context are not identical.

Dallas vs. other major Texas markets (2026 contractor GL ranges)

In brief: Contractor general liability pricing is broadly similar across the four largest Texas metros, but trade mix, project size, and local contract requirements can shift quotes by 10–20% in either direction.

| Texas Metro | Small Business GL (Monthly) | Contractor GL (Monthly) | Common Local Notes |

|---|---|---|---|

| Dallas, TX | $40 to $150 | $150 to $400+ | Heavy commercial build-out and multifamily exposure across DFW |

| Fort Worth, TX | $40 to $140 | $140 to $380+ | More residential and light commercial than Dallas proper |

| Houston, TX | $45 to $160 | $160 to $450+ | Higher hazard exposure from coastal weather, energy, and industrial work |

| Austin, TX | $40 to $150 | $150 to $400+ | Tech build-outs, high-growth residential, and stricter municipal COI wording |

For a deeper city-by-city comparison, see the Fort Worth, Houston, and Austin general liability cost guides.

Dallas GL vs. the Texas state average

In brief: Dallas contractor GL pricing typically runs above the Texas state average because of denser commercial activity, more multifamily and mixed-use build-outs, and stricter project-owner and municipal COI requirements across DFW.

| Benchmark | Typical Monthly GL | Source / Notes |

|---|---|---|

| Texas small business average (all industries) | ~$42 per month | Insureon median, as of 2026 |

| Texas contractor / construction median | ~$71 to $122 per month | Insureon and MoneyGeek Texas medians, as of 2026 |

| U.S. general contractor average | ~$142 per month | Insureon national average for general contractors |

| Dallas, TX contractor range (this guide) | $150 to $400+ per month | ContractorsInsured.net 2026 placement data across 10+ admitted carriers |

The gap between the Dallas range and the broader Texas average is largely driven by trade mix (more GCs and subcontractor-heavy operations in DFW), higher contract limit requirements on commercial and multifamily projects, and additional insured / primary and noncontributory wording that most carriers price into the premium.

Contractor general liability cost by trade in Dallas

In brief: Contractor GL pricing changes by trade because different trades create different claim exposure. A roofer, plumber, GC, electrician, finish contractor, and handyman may all need GL, but they do not carry the same risk.

| Contractor Trade | Expected Pricing Tier | Key Underwriting Concern |

| General contractor | Medium to high | Subcontractor controls, risk transfer, project size, completed operations |

| Roofing contractor | High | Heights, tear-offs, hot work, water intrusion, injury severity |

| Plumbing contractor | Medium to high | Water damage, service work, commercial jobs, completed operations |

| HVAC or electrical contractor | Medium to high | Installation risk, fire or system damage exposure, commercial work |

| Finish trade contractor | Low to medium | Lower hazard work, but property damage and contract requirements still matter |

| Handyman or light repair contractor | Low to medium | Scope of work, excluded operations, revenue, structural or roof work exposure |

Trade classification is one of the biggest reasons two Dallas contractors can receive very different quotes. A small painting contractor with clean loss history and no employees may qualify for a simpler policy. A GC overseeing subcontractors, commercial build-outs, restaurant renovations, multifamily work, or high-value residential projects may need more careful placement. If your business performs several types of work, explain the percentage of each operation. For example, a remodeler who does 70 percent interior finish work, 20 percent light carpentry, and 10 percent plumbing-related work is different from a remodeler who also performs roofing, structural work, excavation, or demolition. This matters because the cheapest policy is not always the safest policy. A policy with exclusions that conflict with your actual work may fail when a GC asks for a COI or when a claim is reported.

Why contractor GL costs more in Dallas

In brief: Contractors usually pay more than office businesses because they work around customers, buildings, equipment, materials, subs, and completed work exposure. Dallas commercial growth, remodeling activity, and North Texas construction demand make correct classification and COI wording important. General liability costs more for contractors because the exposure is more physical. A desk-based business may have limited customer injury or property damage exposure. A contractor can damage flooring, plumbing, walls, roofing systems, fixtures, tenant improvements, landscaping, or commercial property during active work. Dallas contractors may see higher GL premiums because of:

- Jobsite property damage exposure: Contractors often work in homes, restaurants, offices, retail spaces, warehouses, multifamily buildings, and commercial properties. One mistake can cause expensive property damage.

- Completed operations risk: Problems may show up after the job is done. A faulty installation, leak, roof issue, repair defect, or failed component may create a claim later.

- Subcontractor exposure: General contractors and larger trade contractors often rely on subs. Carriers want to know whether subs have their own insurance and whether the contractor uses written agreements.

- Higher-value projects: Commercial build-outs, multifamily work, higher-end residential projects, public-facing properties, and larger North Texas developments can create larger claim potential.

- Contract requirements: Some Dallas contracts may require specific GL limits, additional insured status, primary and noncontributory wording, waiver of subrogation, completed operations wording, business auto, or workers’ comp.

- Trade hazard: Roofing, plumbing, electrical, HVAC, structural work, demolition, excavation, and hot work usually price differently from lower-risk finish trades.

- Claims history: Prior property damage, water damage, injury, construction defect, or completed operations claims can reduce carrier options or increase premium.

The goal is not to buy the cheapest possible general liability policy. The goal is to buy coverage that fits your trade, satisfies the paperwork requirement, and does not create avoidable gaps.

Cost by coverage limit

In brief: Many Dallas contractors start with $1M/$2M general liability limits, but some contracts may require higher limits or special endorsements. The right limit depends on the contract, lease, job owner, GC, municipality, or vendor portal. A common baseline for small businesses and contractors is $1 million per occurrence / $2 million aggregate. This means the policy may pay up to $1 million for a covered occurrence and up to $2 million total during the policy period, subject to policy terms, exclusions, and endorsements.

| Coverage Limit | Common Use Case | Notes |

| $1M per occurrence / $2M aggregate | Common baseline for many small businesses and contractors | Often requested by leases, GCs, owners, vendor portals, and public entities |

| $2M per occurrence / $4M aggregate | Larger contracts, stricter commercial projects, or higher-value work | May be required by certain project owners, landlords, or municipalities |

| Umbrella or excess liability | When required limits exceed the primary GL policy | Can provide additional limits above scheduled underlying policies |

| Project-specific requirement | Municipal, commercial, public-facing, or owner-driven requirements | Contract wording should be reviewed before binding coverage |

A useful Dallas municipal example appears in Dallas City Code Sec. 43-170. In that specific shared dockless vehicle operating permit context, the code requires commercial general liability limits of $1 million for each occurrence and $2 million annual aggregate. It also references additional insured status for the city, business auto when motor vehicles are used, workers’ compensation with statutory limits, employer’s liability, and waiver of subrogation wording. That does not mean every Dallas contractor has the exact same requirement. It shows why municipal, vendor, facility, lease, and project-owner requirements can involve more than just buying a basic GL policy. Before buying coverage, send the contract or certificate instructions to your broker so the policy can be checked against the required wording.

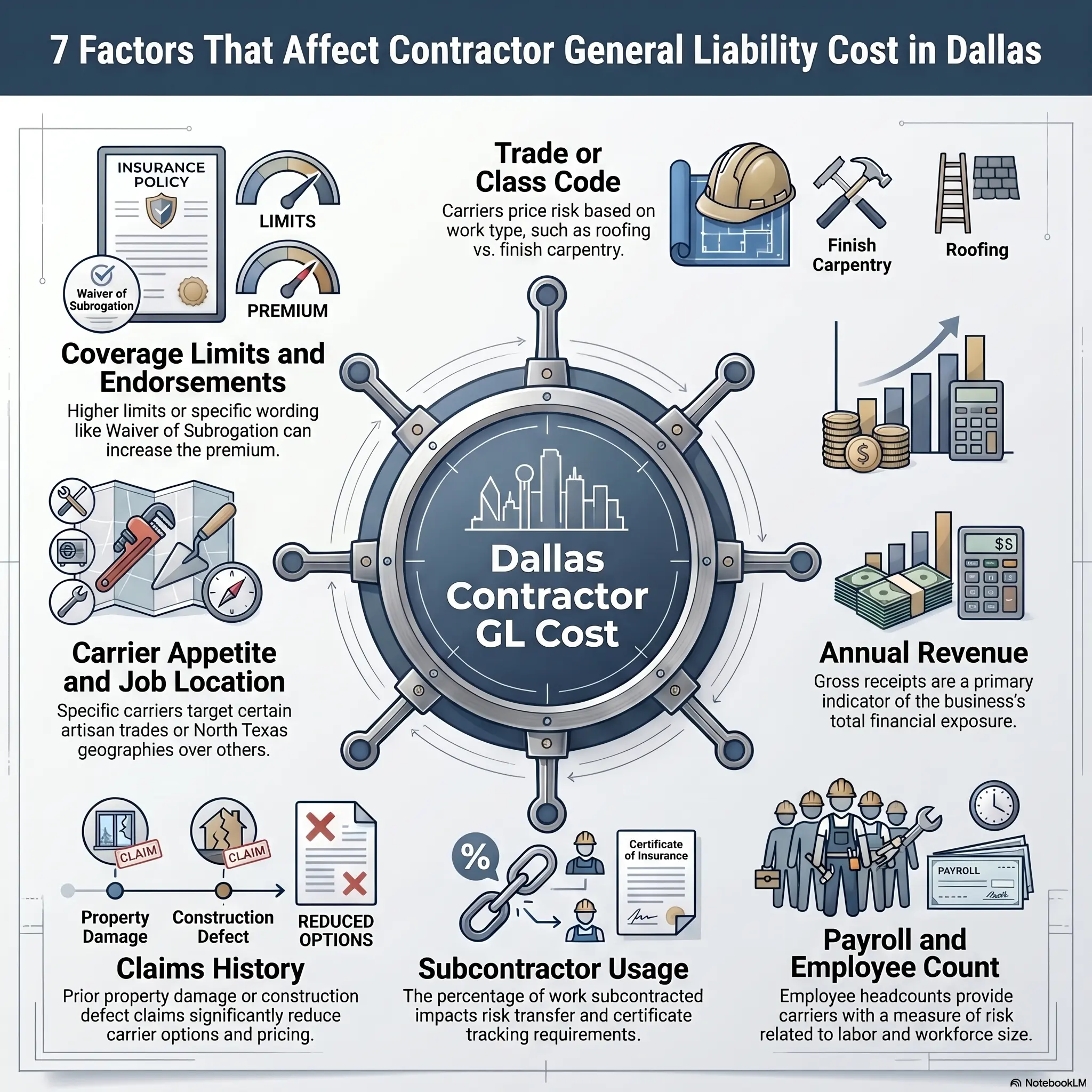

The 7 factors carriers use to price your policy

In brief: Carriers price Dallas general liability policies by looking at the risk behind the business. Your trade, revenue, payroll, subcontractor usage, claims history, limits, endorsements, and job type all affect pricing.

| Factor | Why It Matters | What to Prepare |

| Trade or class code | A roofer, plumber, GC, electrician, and office business do not create the same risk | Clear description of work performed |

| Revenue | Higher sales can mean more operations and more claim exposure | Current and projected annual gross revenue |

| Payroll and employee count | More labor can mean more active jobs and more exposure | Payroll estimate and number of employees |

| Subcontractor usage | Subs can create risk transfer and completed operations issues | Percentage of work subcontracted, COIs from subs, written agreements |

| Claims history | Prior claims may affect eligibility and pricing | Loss runs or claim details from prior policies |

| Limits and endorsements | Higher limits and special wording can affect placement | Contract, lease, bid packet, or vendor portal requirements |

| Carrier appetite and location | Not every carrier wants every contractor class or job type | Current operations, job locations, and prior coverage details |

Here is what each factor means in practical terms.

- Trade or class code: The carrier needs to know what work you actually perform. “Contractor” is too broad. A roofer, plumber, HVAC contractor, electrician, painter, remodeler, and GC may all fall into different underwriting categories.

- Revenue: Many GL policies use gross receipts as part of rating. If revenue is estimated too low, a premium audit may create an additional bill later. The Texas Department of Insurance commercial general liability explainer notes that many CGL policies are auditable and that accurate estimates of payroll, sales, or units are important to avoid additional premium.

- Payroll and employee count: Payroll and employee count help carriers understand how large the operation is and how active the work may be.

- Subcontractor usage: GCs and trade contractors with heavy subcontractor usage may need stronger risk transfer controls. Carriers may ask for subcontractor COIs, written contracts, and proof that subs carry their own coverage.

- Claims history: A clean claims history may help. Prior water damage, jobsite injury, property damage, construction defect, or completed operations claims may increase premium.

- Limits and endorsements: Higher limits, additional insured endorsements, primary and noncontributory wording, waiver of subrogation, and completed operations requirements can affect eligibility and pricing.

- Carrier appetite: Not every insurance carrier wants every contractor. Some carriers are comfortable with artisan trades. Others avoid roofing, structural work, demolition, high subcontractor percentages, or certain commercial operations.

Looking for general liability insurance near me in the DFW Metroplex?

In brief: Contractors searching for “general liability insurance near me” in the Dallas–Fort Worth Metroplex can usually be quoted by a Texas-licensed contractor broker the same day, regardless of whether the job is in Dallas proper or in a surrounding city.

ContractorsInsured.net places contractor coverage across the full DFW Metroplex, including Dallas, Plano, Frisco, McKinney, Richardson, Garland, Mesquite, Irving, Carrollton, Grand Prairie, Arlington, Fort Worth, Allen, Lewisville, and the surrounding Dallas, Collin, Denton, Tarrant, and Rockwall County job sites. Trade classification, revenue, and required limits matter more than the exact city; a roofer working in Plano and a roofer working in South Dallas usually receive similar quotes from the same carrier appetite.

Same-day Certificate of Insurance (COI) for Dallas projects

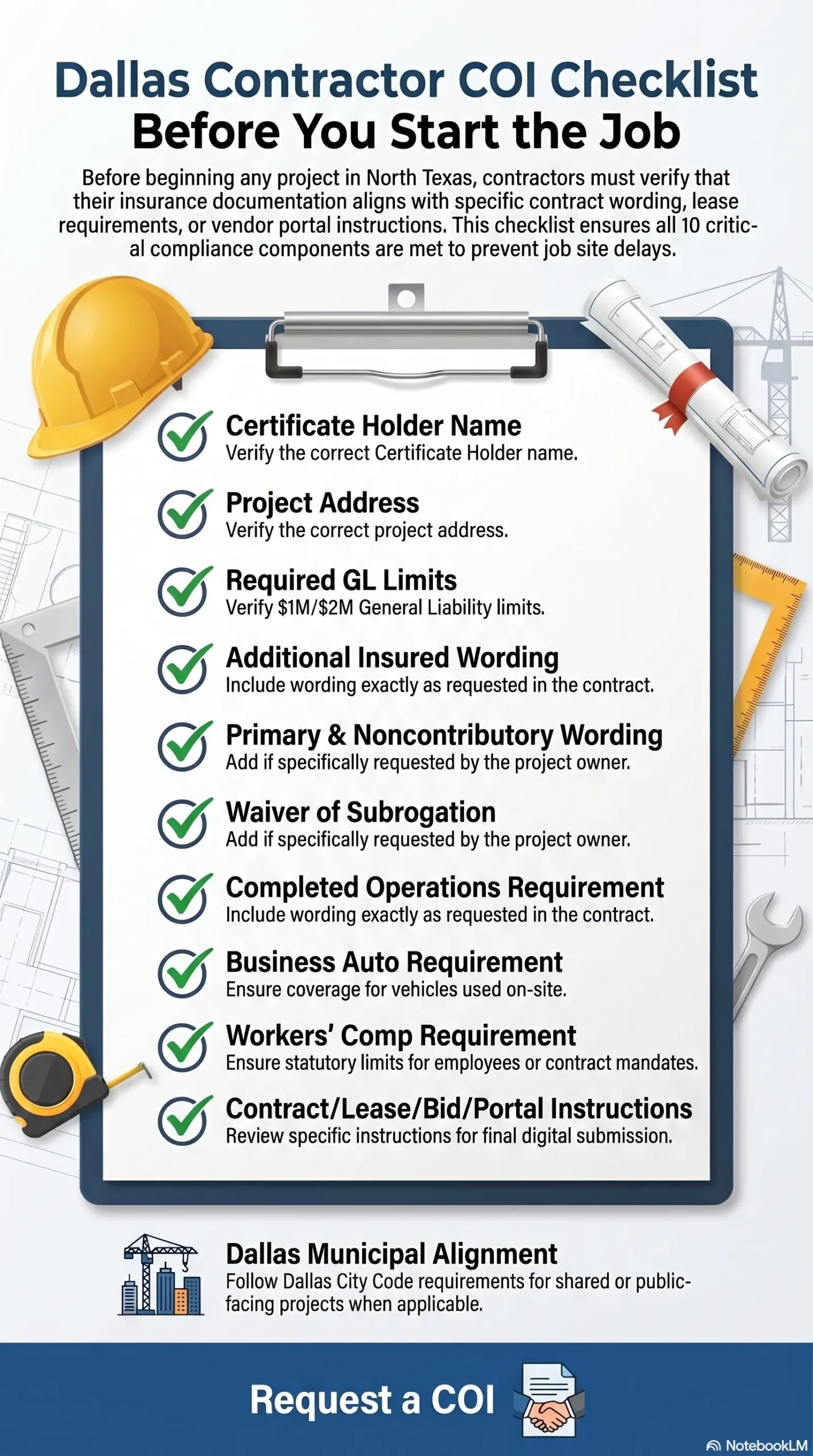

In brief: If your Dallas general liability policy is already active, a same-day Certificate of Insurance can usually be issued within a few hours once the certificate holder, project address, and required wording (additional insured, primary and noncontributory, waiver of subrogation) are confirmed.

Common scenarios where Dallas contractors need a same-day COI include winning a new bid, starting an urgent job for a GC, signing a commercial lease, onboarding into a vendor portal, or satisfying a property manager’s last-minute insurance request. To avoid delays, send the contract or vendor portal instructions to your broker upfront so the COI can be issued correctly the first time. Request a same-day COI.

Dallas contract, lease, and COI requirements

In brief: General liability is not required by Texas law for every Dallas business, but it is commonly required by contracts. Leases, GCs, public entities, commercial clients, and vendor portals often ask for proof of insurance before work starts. A Certificate of Insurance, or COI, is the document that summarizes your coverage for a third party. It usually shows the insured business, insurance carrier, policy number, effective dates, coverage type, limits, and certificate holder. Dallas contractors commonly need a COI when:

- Starting work for a GC

- Signing a commercial lease

- Entering a vendor portal

- Working on a commercial property

- Performing work for a property manager

- Bidding on municipal or public-facing work

- Working in or around a managed property, facility, warehouse, retail site, or multifamily building

- Satisfying a project owner’s insurance requirements

The Dallas City Code example above is useful because it shows how local requirements can combine general liability, business auto, workers’ comp, employer liability, additional insured status, and waiver wording in a specific municipal context. Contractors should not treat that section as a universal rule for every Dallas business, but they should treat it as a reminder to read every contract’s insurance section before starting work. Common COI and endorsement requests may include:

- Certificate of Insurance

- Additional insured endorsement

- Primary and noncontributory wording

- Waiver of subrogation

- Completed operations coverage

- $1M/$2M or higher GL limits

- Specific certificate holder wording

- Business auto liability if vehicles are used for the job

- Workers’ comp if employees are involved or the contract requires it

If a contract asks to add another party to the policy, review the additional insured endorsement request before binding. If the contract asks for subrogation wording, check whether a waiver of subrogation is available. If you already have coverage and only need proof, start with the certificate of insurance process. For broader contractor paperwork support, ContractorsInsured also has a compliance and certificates resource section.

What general liability does not cover

In brief: General liability is important, but it is not a full insurance program. Dallas contractors may also need workers’ comp, commercial auto, tools and equipment coverage, professional liability, or other policies depending on the work. General liability mainly addresses certain third-party liability claims. It does not cover every loss a contractor can face. General liability usually does not cover:

- Employee injuries: Employee injuries are usually handled through workers’ compensation insurance for contractors, if required or purchased.

- Company vehicles: Vehicles used for business usually need commercial auto insurance for contractors.

- Your own tools and equipment: Stolen or damaged tools usually require tools and equipment coverage, inland marine coverage, or property coverage.

- Professional design errors: Design, engineering, consulting, or professional mistakes may require professional liability or errors and omissions coverage.

- Pollution claims: Many GL policies contain pollution exclusions. Certain contractors may need separate pollution liability coverage.

- Intentional acts: Insurance generally does not cover intentional wrongdoing.

- Your own faulty work: GL may respond to resulting property damage in some situations, but it generally does not work like a warranty to replace your defective work.

The Texas Department of Insurance commercial general liability explainer gives examples of CGL exclusions, including damage to your work, damage to your product, contractual liability limitations, workers’ compensation and employer’s liability exclusions, and pollution exclusions. This is why contractors should think in terms of a coverage stack. GL may be the first policy requested by a GC, but it may need to be paired with workers’ comp, commercial auto, tools coverage, bonds, and compliance support.

How Dallas contractors can lower GL costs without creating coverage gaps

In brief: Lowering cost should not mean buying a policy that fails your contract or excludes your real work. The better strategy is to give carriers clean, accurate underwriting information. Dallas contractors can often improve quote quality and avoid delays by preparing the right information before applying. Here are practical ways to control cost:

- Use the correct trade classification. Do not describe your business only as “construction.” Explain whether you are a plumber, roofer, GC, painter, finish carpenter, remodeler, HVAC contractor, electrician, handyman, or another trade.

- Separate lower-risk and higher-risk work. If most of your work is interior finish work, but you sometimes perform roofing, structural work, exterior work, hot work, or plumbing, explain the percentages clearly.

- Keep subcontractor paperwork clean. If you use subs, collect COIs, confirm their limits, require written agreements, and use additional insured wording when appropriate.

- Report accurate revenue. Carriers may audit the policy. Accurate revenue estimates can help prevent surprise premium adjustments later.

- Maintain a clean claims history. Safety procedures, job photos, documentation, written change orders, and quality control can reduce claim frequency.

- Review contracts before binding. Do not buy coverage first and check the contract later. A policy that cannot satisfy the required wording may create delays.

- Avoid lapsed coverage. A clean history of continuous coverage may help underwriting. Lapses can raise questions.

- Bundle only when appropriate. Some businesses benefit from packaging GL with other policies. Contractors with more complex jobsite requirements may need contractor-specific placement.

- Use a contractor-focused broker. Contractors need more than a generic quote. They need help with limits, class codes, COIs, additional insured wording, waivers, and job-specific requirements.

The cheapest policy is not always the best outcome. A slightly cheaper policy that excludes key operations, cannot issue the requested endorsement, or fails a vendor portal can cost more in lost jobs and delays.

What to prepare before requesting a quote

In brief: The faster you provide accurate business, trade, revenue, payroll, subcontractor, and COI details, the faster a broker can quote the right Dallas general liability policy. Before requesting a Dallas general liability quote, gather the following.

| Information Needed | Why the Broker Needs It |

| Legal business name | Needed for applications, policies, underwriting, and certificates |

| DBA, if applicable | Helps match contracts, leases, vendor portals, and certificate requests |

| Business address | Used for rating, mailing, underwriting, and state-specific forms |

| Trade or contractor type | Determines classification and carrier eligibility |

| Description of operations | Helps avoid misclassification and excluded work problems |

| Annual gross revenue | Used by carriers to rate and audit the policy |

| Payroll estimate | Helps carriers understand the size of the operation |

| Employee count | Helps identify risk and possible workers’ comp needs |

| Subcontractor percentage | Important for GCs and trade contractors who use subs |

| Claims history | Prior claims can affect eligibility and premium |

| Desired limits | Many businesses start with $1M/$2M, but contracts may require more |

| Contract or bid packet | Shows exact COI and endorsement wording |

| Certificate holder information | Needed for accurate COI issuance |

| Additional insured wording | Required when a GC, owner, landlord, city, or property manager must be added |

| Vehicle use | Helps determine whether commercial auto is needed |

| Job locations | Helps underwriters understand where work is performed |

If the job is deadline-driven, send the contract, lease, bid packet, or vendor portal instructions when you request the quote. That allows the broker to confirm whether the policy can satisfy the wording before coverage is bound. The ContractorsInsured.net homepage states that the brokerage works with roofing, general, and plumbing contractors in California and Texas and helps with general liability, workers’ comp, commercial auto, COIs, additional insured, primary and noncontributory, and waiver of subrogation requirements. If you want to compare Dallas pricing with other Texas markets, you can also review theHouston general liability insurance cost guide and theFort Worth general liability insurance cost guide. Get a Quote

Key terms for Dallas contractors

- COI (Certificate of Insurance): A summary document showing your active coverage, used to satisfy GCs, landlords, vendor portals, and project owners.

- Additional insured: Another party (such as a GC, owner, or property manager) named on your policy for certain covered claims tied to your work.

- Primary and noncontributory: Wording that makes your policy respond first, before another party’s policy, for covered claims.

- Waiver of subrogation: A clause where your insurer agrees not to pursue recovery from another party (often required by GCs and municipalities).

- Completed operations: Coverage that may respond to claims arising after a job is finished, such as a defect or leak discovered later.

- $1M/$2M limits: $1 million per occurrence and $2 million aggregate, the most common baseline for Dallas contracts.

- Premium audit: A carrier review of payroll, revenue, or subcontractor costs after the policy year that can result in an additional bill or refund.

Frequently asked questions

In brief: These FAQs answer the questions Dallas contractors usually ask before requesting a general liability quote. They are also written for FAQ schema and AI answer extraction.

How much does general liability insurance cost in Dallas, Texas?

General liability insurance in Dallas, Texas often costs around $40 to $150 per month for lower-risk small businesses. Many contractors should budget closer to $150 to $400+ per month, depending on trade, revenue, payroll, subcontractor usage, claims history, limits, endorsements, and job requirements.

Is general liability insurance legally required in Dallas?

General liability insurance is not required by Texas law for every Dallas business as a blanket rule. However, many contracts, leases, GCs, project owners, public entities, vendor portals, and commercial clients require proof of GL before work begins. Contractors often need it to bid, lease space, or access job sites.

What limits do Dallas contracts commonly require?

Many Dallas contracts commonly ask for at least $1 million per occurrence and $2 million aggregate in general liability coverage. Some contracts may also require additional insured status, primary and noncontributory wording, waiver of subrogation, completed operations coverage, business auto, workers’ comp, or higher limits.

Why might Dallas contractor GL cost more than a basic office policy?

Dallas contractor GL can cost more because contractors create more physical risk. Jobsite work can involve property damage, customer injury, completed operations claims, subcontractor exposure, ladders, tools, water lines, electrical systems, roofing, structural work, and commercial property exposure.

Does Dallas contractor GL cover tools, autos, or employee injuries?

No. General liability usually does not cover your own tools, company vehicles, or employee injuries. Tools may need tools and equipment coverage, vehicles usually need commercial auto, and employee injuries are usually handled through workers’ compensation if required or purchased.

What does additional insured mean on a Dallas contractor COI?

Additional insured status means another party, such as a GC, owner, landlord, property manager, or municipality, may receive certain protection under your policy for covered claims. A COI may show the request, but the actual additional insured endorsement should match the contract requirements.

How fast can I get a COI for a Dallas project?

Often, proof of insurance can be issued quickly if coverage is active and the requested wording is available. The process is faster when you provide the certificate holder name, project address, contract requirements, additional insured wording, waiver request, and vendor portal instructions upfront.

What information do I need before requesting a Dallas GL quote?

You should have your legal business name, trade, business address, annual revenue, payroll, employee count, subcontractor percentage, claims history, desired limits, contract wording, certificate holder details, and job locations ready. Contractors should also explain whether they perform roofing, plumbing, electrical, HVAC, structural, demolition, or subcontracted work.

Get a Dallas general liability quote

In brief: The right Dallas general liability policy should match your trade, contract wording, COI requirements, and real jobsite exposure. Do not buy coverage based only on the lowest monthly number. If you need general liability insurance for a Dallas job, lease, bid, vendor portal, municipal requirement, or contractor requirement, ContractorsInsured.net can help you compare options and prepare the right paperwork. A good quote should answer four questions:

- Does the policy match the work you actually perform?

- Does it satisfy the contract, lease, GC, city requirement, property manager, or vendor portal?

- Can the broker issue the COI and endorsements you need?

- Are there exclusions or gaps that could hurt you later?

ContractorsInsured.net helps contractors with general liability, workers’ comp, commercial auto, COIs, additional insured endorsements, primary and noncontributory wording, waiver of subrogation, and other compliance requirements. Get a Quote Disclaimer: This article is general information, not legal advice. Coverage, eligibility, forms, endorsements, limits, exclusions, and pricing vary by carrier and underwriting approval. Always review your policy and contract requirements with a licensed insurance professional before binding coverage.