How Much Does General Liability Insurance Cost in Oakland, California? 2026 Guide

[HERO: general-liability-insurance-cost-oakland-california-contractor-general-liability-insurance.webp]

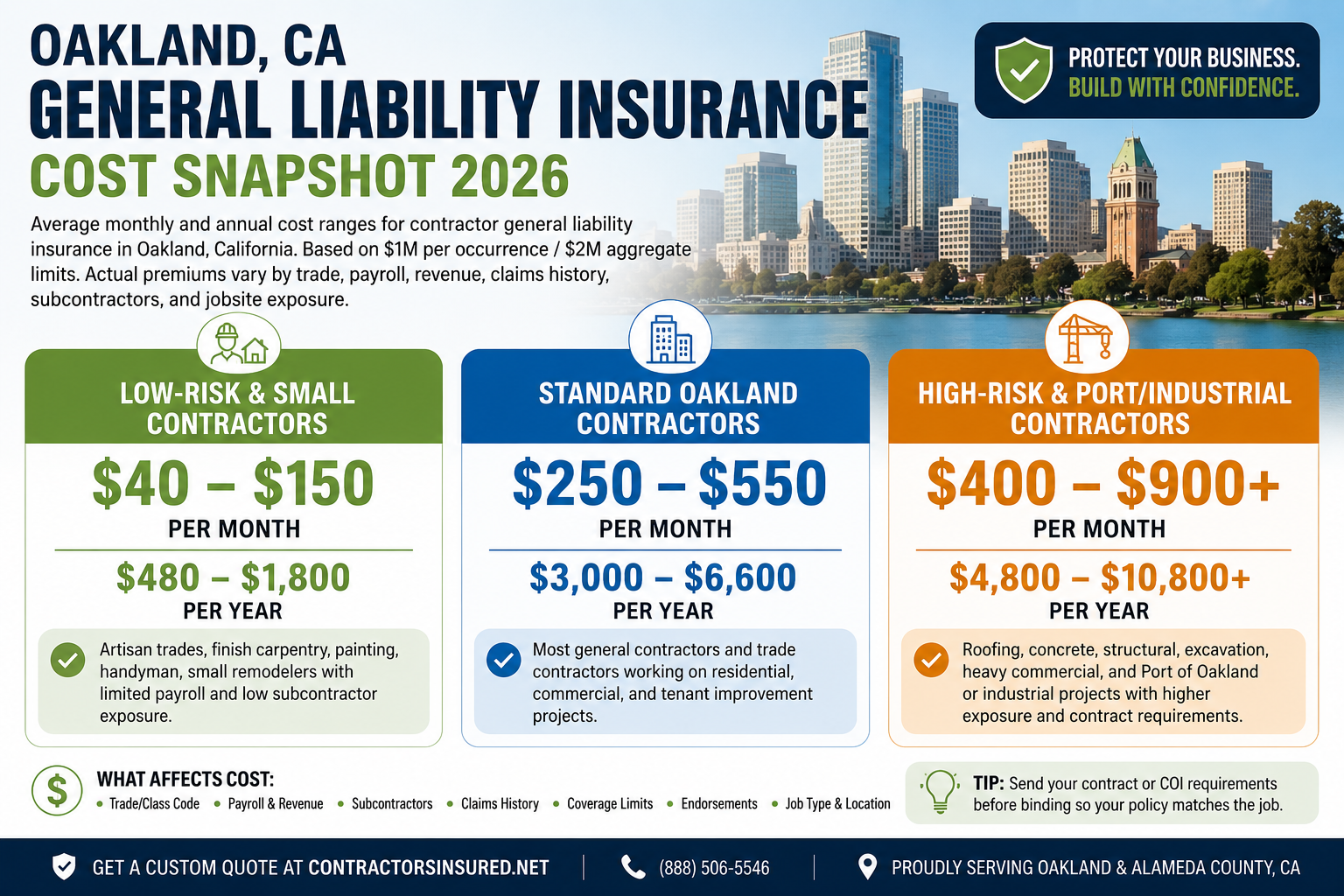

Most Oakland general contractors typically pay $250 to $550 per month ($3,000 to $6,600 per year) for a standard $1M per occurrence / $2M aggregate general liability policy, with roofers, structural trades, Port-adjacent contractors, and contractors on high-value East Bay commercial projects often paying more. The final premium depends on trade class, payroll, subcontractor cost, gross receipts, prior claims, required endorsements, and whether the job involves downtown infill, Lake Merritt commercial space, Port of Oakland work, or municipal requirements. A small finish contractor may land below the Oakland midpoint, while a roofing, concrete, structural, or heavy commercial contractor may need higher limits, broader endorsements, or umbrella coverage. Use the ranges below as planning numbers, then quote against the exact contract, lease, or COI request. As ContractorsInsured.net (CA Lic #6015321), we shop multiple California-admitted carriers for Oakland contractors, quote the same business day, and issue the COI right after binding.

What Oakland contractors are actually trying to solve

In brief: Oakland contractors are usually not asking whether GL exists. They are trying to price a policy, satisfy a contract, and avoid COI rejection.

Most Oakland contractors searching for general liability costs want a fast, locally credible answer: monthly cost, annual cost, what affects pricing, which limits are normal, and what a GC, landlord, vendor portal, Port requirement, or City of Oakland contract may ask for.

That matters because AI summaries now intercept many informational searches. Pew Research Center found that Google users were less likely to click traditional links when an AI summary appeared. The practical win condition is not only ranking. It is becoming the clear, quotable, cited source that an AI answer can lift when a contractor asks how much general liability insurance costs in Oakland.

Oakland also deserves a different answer than a generic national average. The East Bay combines infill residential work in Rockridge and Temescal, Lake Merritt and downtown commercial projects, industrial work near East Oakland and Jack London Square, and Port of Oakland or airport-adjacent operations. Those exposures can change underwriting, endorsements, and limits.

What general liability insurance covers

In brief: General liability protects against third-party bodily injury, third-party property damage, personal and advertising injury, and completed operations claims, subject to the policy terms, limits, and exclusions.

General liability insurance is a third-party liability policy that responds to claims arising from a business’s operations, including bodily injury to non-employees, property damage to third parties, and personal and advertising injury. For contractors, it is the most commonly required coverage in contracts, leases, vendor portals, and city permit packets.

For Oakland contractors, general liability is the policy a GC, property owner, landlord, public agency, or commercial client usually asks for first. It is why general liability insurance for contractors is often the foundation of a contractor insurance package before workers’ compensation, commercial auto, tools and equipment, builder’s risk, or umbrella coverage are added.

The California Department of Insurance describes Commercial General Liability as the standard commercial liability policy used to insure businesses and explains that it commonly includes premises liability, products liability, and completed operations coverage. The SBA also explains that general liability insurance may respond to bodily injury, property damage, medical expenses, libel, slander, lawsuit defense, settlements, and judgments.

Scenario card 1: Oakland warehouse jobsite injury

A delivery driver arrives at an Oakland warehouse project and trips over unsecured materials near the loading area. The driver breaks an ankle and files a bodily injury claim. General liability may respond to the third-party injury claim and defense costs, depending on fault, policy language, and exclusions.

Scenario card 2: Berkeley remodel property damage

A plumbing crew working on a Berkeley remodel cracks a homeowner’s tile floor while moving equipment through a finished hallway. General liability may respond to third-party property damage, but the policy must be reviewed carefully if the damage involves the contractor’s own work or materials.

Scenario card 3: Emeryville advertising injury

An Emeryville subcontractor posts a copyrighted jobsite photo on its website and social media without permission. The photographer sends a demand letter. Personal and advertising injury coverage may respond to certain copyright or advertising injury allegations, subject to exclusions.

Scenario card 4: Alameda completed operations leak

An Alameda roofing crew finishes a project. Six months later, a leak causes interior water damage to the customer’s property. Completed operations coverage may matter because the alleged damage happened after the work was finished.

Scenario card 5: Piedmont subcontractor lawsuit

A Piedmont general contractor is named in a lawsuit over a subcontractor’s work. Even if the GC did not perform the faulty work directly, defense costs can become expensive quickly. General liability may help defend covered third-party claims, subject to the policy terms.

How much does general liability insurance cost in Oakland?

In brief: Most Oakland general contractors should budget $250 to $550 per month for a standard $1M/$2M GL policy, while higher-risk trades and Port-adjacent work can run $400 to $900+ per month.

Most Oakland general contractors typically pay $250 to $550 per month, or $3,000 to $6,600 per year, for a standard $1M per occurrence / $2M aggregate general liability policy.

That range is higher than a low-risk national online quote because Oakland is not a low-exposure market for many contractors. Bay Area labor costs, dense infill work, older properties, high-value commercial spaces, and East Bay contract requirements all affect underwriting. Unlike national aggregators that advertise $40 to $150 per month for a generic small business, Oakland contractor pricing often reflects trade-specific risk, subcontractor exposure, project size, and the exact COI language required by the job.

For statewide context, general liability insurance for California contractors can help compare Oakland against broader California contractor GL expectations. For a deeper policy foundation, see what general liability covers.

Oakland contractor profile | Typical monthly GL cost | Typical annual GL cost | Notes |

|---|---|---|---|

Low-risk finish contractor, small artisan trade | $90 to $250 | $1,080 to $3,000 | Lower payroll, smaller jobs, limited subcontractor exposure |

Standard Oakland general contractor | $250 to $550 | $3,000 to $6,600 | Common planning range for $1M/$2M limits |

Plumbing, electrical, HVAC, tenant improvement | $175 to $500 | $2,100 to $6,000 | Pricing depends on operations, permits, and completed operations exposure |

Concrete, structural, framing, excavation | $350 to $850 | $4,200 to $10,200 | Higher severity exposure and jobsite risk |

Roofing contractor | $400 to $900+ | $4,800 to $10,800+ | Roofing is often one of the most expensive GL classes |

Port-adjacent, airport-adjacent, heavy commercial, or industrial contractor | $500 to $1,200+ | $6,000 to $14,400+ | Contract wording, higher limits, auto, pollution, and umbrella may affect final pricing |

A contractor working only on small residential repairs in Fruitvale or San Leandro may not price the same as a GC managing subcontractors on a downtown Oakland commercial buildout. A contractor near the Port of Oakland may also face contract requirements that involve higher limits, specific additional insured language, waiver wording, and completed operations requirements.

Why contractor GL costs more in Oakland and the East Bay

In brief: Oakland pricing reflects Bay Area claim severity, dense infill jobsites, Port and industrial exposure, high-value property, and contract language that often goes beyond a basic certificate.

Oakland general liability insurance costs more than many inland California metros because the exposure is different. A $1M property damage claim can become more plausible when work happens in dense commercial corridors, high-value homes, older multifamily properties, tight mixed-use buildings, or industrial sites with expensive adjacent operations.

The Port of Oakland also changes the conversation. The Port’s official supplier insurance requirements show Commercial General Liability is required for suppliers performing work, with limits including $1M per occurrence and $2M annual general aggregate, plus additional insured and waiver of subrogation language in favor of the additional insured. Some City of Oakland documents also require higher limits. One 2026 City Schedule Q example requires CGL of not less than $2M each occurrence and states that additional insured status on an ACORD certificate alone is insufficient proof of meeting the endorsement requirement.

“Oakland contractors are not priced only on trade class. Carriers also look at where the work is performed, who controls the jobsite, how many subcontractors are involved, and whether the certificate request adds Port, municipal, or East Bay commercial language that must be endorsed correctly.”

Pascal Burke, Licensed Insurance Broker (CA #6015321, TX #3305690)

The density of infill construction matters. A crew working in Rockridge, Temescal, Lake Merritt, downtown Oakland, Emeryville, or Berkeley often works close to tenants, pedestrians, neighboring businesses, parked vehicles, and finished property. That raises the chance that a small error becomes a third-party property damage or bodily injury claim.

Oakland’s East Bay litigation environment also matters. Defense costs can be significant even when a contractor disputes liability. A properly structured GL policy is not just about paying damages. It is also about defense, endorsements, and whether the policy aligns with the contract before work starts.

Cost by coverage limit

In brief: $1M/$2M is the common baseline, but Oakland commercial, municipal, Port, and high-value projects may require $2M/$4M, $5M total limits, or umbrella coverage.

Most small and midsize Oakland contractors start with $1M per occurrence and $2M aggregate general liability limits. That is the most common baseline seen in many commercial leases, subcontract agreements, and vendor portals. However, it is not always enough.

For larger commercial projects, municipal contracts, property management accounts, and certain Port-adjacent jobs, the required limit may rise to $2M per occurrence, $4M aggregate, or $5M combined with umbrella or excess liability. City and Port language may also require endorsements that a basic policy does not automatically include.

Coverage structure | Typical Oakland use case | Estimated monthly cost impact | Notes |

|---|---|---|---|

$1M occurrence / $2M aggregate | Standard small contractor baseline | Base range | Common starting point for many GCs and subcontractors |

$2M occurrence / $4M aggregate | Larger East Bay commercial projects | Moderate increase | May be required by landlords, GCs, or municipal contracts |

$1M/$2M plus $1M umbrella | Contracts requiring higher total limits | Moderate to high increase | Umbrella may sit over GL and other eligible policies |

$1M/$2M plus $5M umbrella | Port, public agency, large commercial, or institutional jobs | High increase | Underwriting may review trade, payroll, auto, prior losses, and contract language |

Project-specific or wrap/OCIP/CCIP arrangement | Large controlled insurance program projects | Varies | Contractor may still need offsite GL, auto, tools, pollution, or excluded operations coverage |

For contractors comparing Bay Area pricing, the general liability insurance cost in San Jose guide can help separate Oakland’s Port and East Bay infill context from South Bay tech-campus and commercial buildout exposure. For Southern California comparison, see general liability insurance cost in Los Angeles.

The 7 factors carriers use to price your policy

In brief: Carriers price Oakland GL by class code, payroll, revenue, subcontractor cost, job type, prior losses, limits, endorsements, and how well the application matches the real work.

A carrier does not price a contractor only by city. Oakland matters, but it is one rating factor among many. The final premium is built from the contractor’s operations, job mix, payroll, receipts, subcontractor use, coverage limits, and loss history.

Pricing factor | Why it affects Oakland GL cost | Example |

|---|---|---|

Trade classification | Some trades create more severe bodily injury, property damage, or completed operations exposure | Roofing, structural, excavation, and concrete usually cost more than low-risk finish work |

Gross receipts | Higher revenue usually means more work volume and more exposure | A $1.8M contractor usually pays more than a $250K contractor |

Payroll | Payroll helps carriers estimate labor exposure | More field payroll can increase premium |

Subcontractor cost | GCs with uninsured or poorly insured subs create additional risk | Carriers may ask for subcontractor COIs and written agreements |

Job type | Residential, commercial, public works, industrial, and Port-adjacent work price differently | A Port-adjacent industrial project may need more review than a small residential repair |

Prior claims | Loss history is a major underwriting signal | A recent water damage or injury claim can affect eligibility and rate |

Limits and endorsements | Higher limits and contract wording can increase cost | Additional insured, primary and noncontributory, waiver of subrogation, and completed operations language may matter |

The Insurance Information Institute explains that a commercial general liability policy can protect against property damage, bodily injury, and personal and advertising injury caused by business operations or employees. For contractors, the underwriting question is not only what CGL covers. It is how risky the contractor’s operations look when the carrier applies trade classification, jobsite exposure, and loss history.

Oakland contract, lease, and COI requirements

In brief: Oakland contractors should quote from the contract, not memory, because the COI often needs exact limits, additional insured wording, primary language, and waiver endorsements.

A Certificate of Insurance is not the policy. It is evidence of coverage at a point in time. The endorsement wording behind it is often what decides whether the GC, landlord, public agency, vendor portal, or Port contract accepts or rejects the certificate.

Start with Certificate of Insurance basics if you need a plain-English overview before sending a COI request. For Oakland jobs, the common contract requirements include:

$1M/$2M general liability limits, or higher limits for larger work.

Additional insured status for the project owner, GC, landlord, City, Port, or related parties.

Primary and noncontributory wording.

Waiver of subrogation, when required.

Completed operations coverage for a stated period after project completion.

Commercial auto coverage if vehicles are used.

Workers’ compensation and employer’s liability if employees are involved.

Umbrella or excess liability when the required limits exceed the base GL policy.

The official Port of Oakland Supplier Insurance Requirements show Commercial General Liability required for suppliers performing work and include additional insured and waiver wording. City of Oakland Schedule Q language can require commercial general liability, automobile liability, workers’ compensation, professional liability when applicable, and additional insured endorsements. The City of Oakland Risk Management page also states that risk management services provide contract insurance requirements review.

For endorsement-specific help, review the Additional Insured endorsement page and the Waiver of Subrogation page before binding. These details are not clerical. They can decide whether you are cleared to mobilize.

What general liability does NOT cover

In brief: General liability is essential, but it does not replace workers’ compensation, commercial auto, tools coverage, builder’s risk, E&O, or umbrella coverage.

General liability is broad, but it is not all-risk insurance. The California Department of Insurance notes that major CGL exclusions may include workers’ compensation, employer’s liability, pollution, auto, care, custody and control, damage to your work, and other excluded exposures.

For Oakland contractors, the most important gaps are:

Employee injuries. Workers’ compensation, not GL, responds to employee jobsite injuries.

Business vehicles. Commercial auto is needed for covered vehicles, hired autos, and non-owned auto exposures.

Your tools and equipment. Inland marine or tools and equipment coverage is usually needed for theft or damage to contractor property.

Professional mistakes. Design, consulting, estimating, or professional errors may require E&O coverage.

Damage to your own work. GL may respond to resulting third-party damage, but it commonly excludes the cost to repair or replace your own faulty work.

Builder’s risk exposures. A project under construction may need builder’s risk for covered property losses during the course of construction.

Higher-than-policy claims. Umbrella or excess liability may be needed when contracts require limits above the base policy.

CSLB workers’ compensation requirements are separate from general liability. CSLB states that workers’ compensation coverage must be continuous and that failure to maintain required coverage can result in license suspension. DIR also states that public works projects can trigger prevailing wage, apprenticeship, registration, and enforcement requirements. For a broader state compliance view, see California contractor GL requirements.

How Oakland contractors can lower GL costs without creating coverage gaps

In brief: The safest savings come from cleaner underwriting, accurate class codes, documented subcontractors, better contracts, loss control, and quoting before the COI deadline.

Cheaper is not always better. A policy that saves $60 per month but excludes your main operation, refuses your required additional insured wording, or cannot support a same-day COI can cost far more than it saves.

Use these steps to reduce premiums without weakening the policy:

Classify the work correctly. Do not let a cheaper but inaccurate class code create a denial problem later.

Separate payroll by trade when possible. If your payroll records clearly separate lower-risk and higher-risk operations, underwriting may be cleaner.

Collect subcontractor COIs before work starts. Require GL, workers’ comp when applicable, auto if vehicles are involved, and matching endorsements.

Use written contracts with subs. Written risk transfer can help underwriting and claim defense.

Fix jobsite safety issues early. Loss control, photos, training, and documented procedures can help reduce claims.

Avoid last-minute COI requests. Rushed certificates create endorsement mistakes.

Review deductibles and self-insured retentions. Higher retentions may reduce premium but can create cash-flow risk after a claim.

Quote with a multi-carrier broker. Contractor appetite changes by carrier, class, and region.

For many general contractors, the best savings strategy is not lowering limits. It is matching the policy to the contracts they actually sign, then using clean records to avoid unnecessary underwriting penalties.

What to prepare before requesting a quote

In brief: The fastest Oakland GL quotes come from complete applications, accurate payroll and revenue, current loss runs, subcontractor details, and the exact COI wording.

A contractor who sends only “I need GL” will usually get a slower and less accurate quote. A contractor who sends revenue, payroll, trade description, subcontractor cost, license information, contracts, and COI wording gives the broker and carrier enough detail to quote the right policy.

Quote item | Why it matters | What to send |

|---|---|---|

Legal business name and DBA | Policy must match contracts and license records | Entity name, DBA, mailing address, FEIN if available |

CSLB license number | Helps confirm trade classification and compliance | Active CSLB license number and classifications |

Trade description | Determines carrier appetite and class code | Exact work performed and work excluded |

Annual gross receipts | Helps calculate exposure | Last 12 months and projected next 12 months |

Payroll | Used in rating and audit | Owner payroll, employee payroll, field payroll |

Subcontractor cost | Important for GCs and larger jobs | Annual subcontractor spend and COI collection process |

Prior claims or loss runs | Underwriting reviews loss history | 3 to 5 years of loss runs, if available |

Current policy | Helps compare coverage | Declarations page and endorsements |

Contract or COI request | Prevents rejected certificates | Full insurance requirements, not just a screenshot |

Vehicle and equipment exposure | GL does not cover all auto or tools risk | Vehicle list, equipment values, jobsite storage details |

“The fastest way to get an Oakland contractor quote approved is to send the insurance requirements before the policy is bound. If the contract asks for additional insured, primary and noncontributory, waiver of subrogation, or completed operations wording, we want to solve that upfront, not after the certificate is rejected.”

Pascal Burke, Licensed Insurance Broker (CA #6015321, TX #3305690)

Need help now? Start with Get an Oakland GL quote. Existing ContractorsInsured.net clients who only need proof of coverage can use Request a COI for an Oakland job.

Frequently asked questions about general liability insurance cost in Oakland CA

In brief: The FAQs below are written for quick answers on Oakland GL pricing, requirements, COIs, Port work, CSLB compliance, and quote preparation.