Last updated: June 2026

Reviewed by: Pascal Burke, Licensed Insurance Broker, CA License #6015321, TX License #3305690

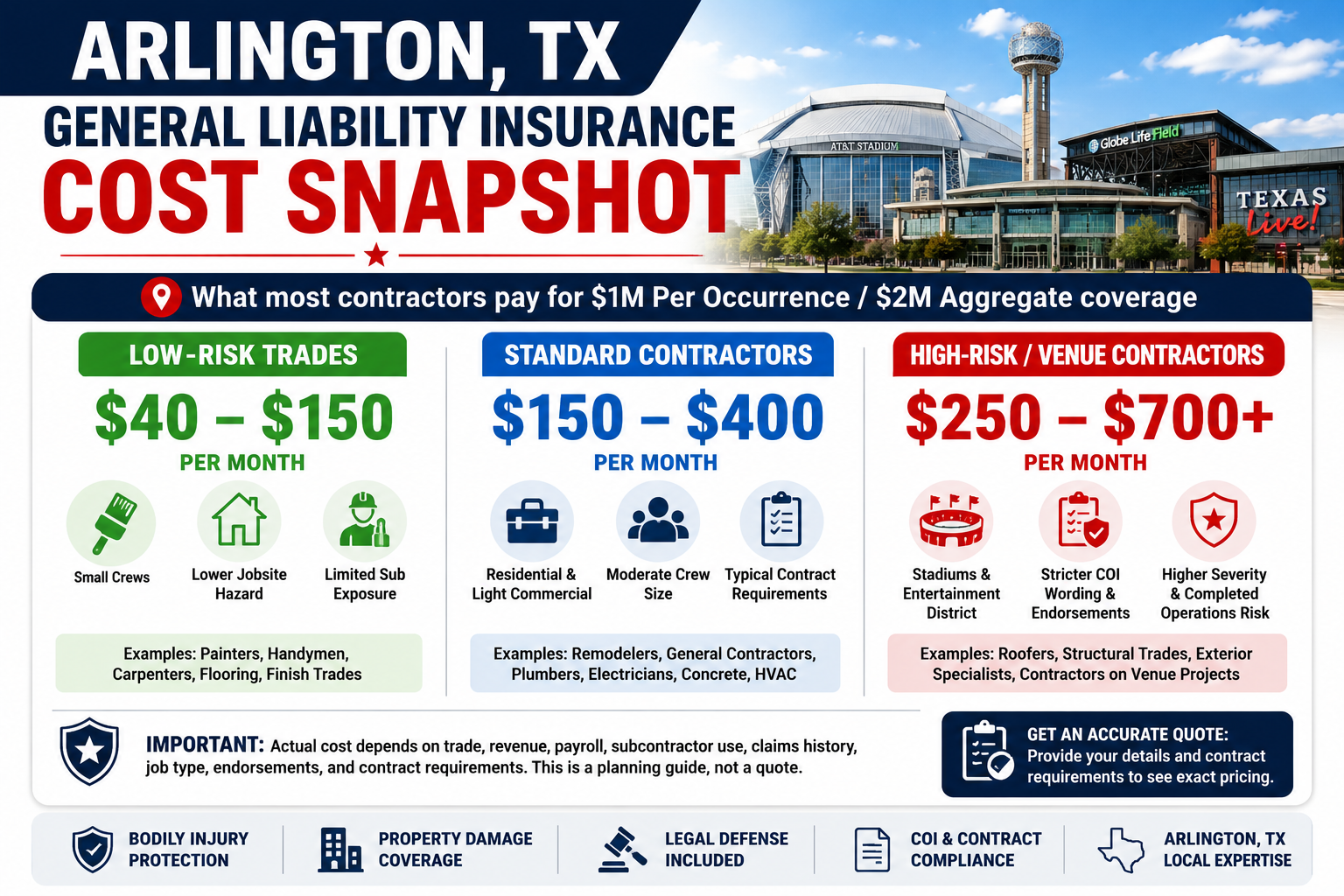

Most Arlington general contractors typically pay $150 to $400 per month ($1,800 to $4,800 per year) for a standard $1M per occurrence / $2M aggregate general liability policy, with roofers, structural trades, and contractors on stadium, convention center, or entertainment-venue projects often paying more. Smaller low-risk trades may see pricing closer to $40 to $150 per month, while contractors working near AT&T Stadium, Globe Life Field, Texas Live!, Six Flags Over Texas, Hurricane Harbor, or Arlington Convention Center may need higher limits, stricter COI wording, and endorsements that increase premium. The fastest way to price accurately is to match your trade, payroll, revenue, subcontractor use, prior claims, and contract requirements to the right carrier before you bind. As ContractorsInsured.net (TX Lic #3305690), we shop multiple Texas-admitted carriers for Arlington contractors, quote the same business day, and issue the COI right after binding.

What general liability insurance covers

In brief: General liability covers third-party injury, third-party property damage, personal and advertising injury, completed operations, and legal defense, subject to policy terms, exclusions, limits, and endorsements.

General liability insurance is a third-party liability policy that responds to claims arising from a business’s operations, including bodily injury to non-employees, property damage to third parties, and personal and advertising injury. For contractors, it is the most commonly required coverage in contracts, leases, vendor portals, and city permit packets.

For Texas contractors, TDI’s CGL coverage summary describes commercial general liability as protection against claims involving bodily injury, property damage, and personal and advertising injury, including premises and operations coverage and products-completed operations coverage. The SBA business insurance overview also identifies general liability as protection against financial loss from bodily injury, property damage, medical expenses, libel, slander, lawsuits, settlements, and judgments.

For Arlington contractors, this matters because jobsite exposure is rarely limited to the property owner. A subcontractor, delivery driver, tenant, venue representative, pedestrian, inspector, or neighboring property owner can become part of a claim. A well-built contractor general liability policy is designed to respond when a third party alleges that your operations caused covered damage or injury.

Scenario card 1: Stadium-area jobsite injury

A material delivery driver trips over loose debris at an Arlington stadium-area jobsite and breaks an ankle. If the driver is not your employee and alleges your crew created the hazard, general liability may respond to the bodily injury claim and defense costs.

Scenario card 2: Pantego remodel property damage

A plumbing crew working on a Pantego remodel cracks the homeowner’s tile floor while moving equipment through the house. General liability may respond to third-party property damage, depending on the facts, exclusions, and whether the damaged property is part of the contractor’s own work.

Scenario card 3: Grand Prairie advertising injury

A Grand Prairie subcontractor uses a copyrighted jobsite photo in a marketing post without permission. If a copyright or advertising injury claim follows, Coverage B may apply if the claim fits the policy language and is not excluded.

Scenario card 4: Mansfield completed operations

A Mansfield roofing crew finishes a project. Six months later, a leak causes interior drywall and flooring damage. General liability may respond to resulting third-party property damage under products-completed operations coverage, while the cost to redo the roof itself may be excluded.

Scenario card 5: Arlington Convention Center vendor lawsuit

A general contractor working through an Arlington Convention Center vendor packet is named in a lawsuit over a subcontractor’s work. General liability may pay defense costs even when liability is disputed, subject to policy terms and available limits.

The key is not just having a policy. It is having the right classification, completed operations coverage, subcontractor controls, and endorsements for the actual work your Arlington business performs.

How much does general liability insurance cost in Arlington?

In brief: Most Arlington contractors should budget $150 to $400 per month for standard $1M/$2M GL, while lower-risk trades may pay less and higher-risk venue, roofing, or structural contractors may pay more.

Most Arlington general contractors typically pay $150 to $400 per month ($1,800 to $4,800 per year) for a standard $1M per occurrence / $2M aggregate general liability policy.

That range fits many remodelers, residential general contractors, finish trades, small commercial contractors, and mid-Cities construction businesses with clean loss history. Arlington pricing is often close to Texas median contractor pricing, but the local mix matters. A contractor doing residential infill near UT Arlington is not priced the same as a contractor with a stadium district vendor packet requiring higher limits, Additional Insured wording, Primary Noncontributory language, and Waiver of Subrogation.

Arlington contractor profile | Common monthly range | Common annual range | Why pricing moves |

|---|---|---|---|

Low-risk artisan or finish trade | $40 to $150 | $480 to $1,800 | Smaller crews, lower jobsite hazard, limited subcontractor exposure |

Standard Arlington general contractor | $150 to $400 | $1,800 to $4,800 | Remodels, small commercial work, residential and light commercial mix |

Roofing, structural, or exterior contractor | $250 to $700+ | $3,000 to $8,400+ | Height, water intrusion, completed operations, and severity potential |

Stadium, convention, or entertainment-venue contractor | $250 to $700+ | $3,000 to $8,400+ | Higher-value venues, stricter COI wording, and possible excess requirements |

Contractor with prior claims or poor subcontractor controls | Varies widely | Varies widely | Loss history, uninsured subs, contract risk, and classification issues |

These are planning ranges, not guaranteed quotes. Carriers still underwrite revenue, payroll, trade class, job type, subcontractor costs, prior losses, location, and requested endorsements. A small contractor with $100,000 in annual receipts may price very differently from a $2 million general contractor coordinating multiple subcontractors around Tarrant County.

Trade or business type | Arlington pricing tendency | Notes |

|---|---|---|

Handyman or small repair contractor | Lower to moderate | Depends on scope, licensing needs, and whether structural, roofing, plumbing, or electrical work is included |

Interior remodeler | Moderate | Pricing rises with subcontractor use, occupied-property work, and higher project values |

General contractor | Moderate to higher | GC pricing reflects contractual risk and supervision of subcontractors |

Roofing contractor | Higher | Height exposure and completed operations risk often push premiums above baseline |

Plumbing contractor | Moderate to higher | Water damage potential and work inside finished property increase severity |

Concrete or masonry contractor | Moderate to higher | Slip, trip, structural, and equipment exposures influence rating |

Venue or event build-out contractor | Higher | Stadium, entertainment, and convention center contracts may require endorsements and higher limits |

Unlike generic aggregator pages and statewide contractor-specific competitors such as affordablecontractorsinsurance.com, this guide ties the cost range to Arlington’s stadium district, mid-Cities location, city vendor insurance requirements, and real contractor COI issues.

If you are comparing Arlington against nearby markets, see the separate guides to general liability insurance cost in Dallas and general liability insurance cost in Fort Worth.

Why contractor GL pricing reflects DFW outer-ring reality in Arlington

In brief: Arlington GL pricing sits between residential mid-Cities contracting and higher-stakes entertainment district contracting, so the same trade can price differently depending on contracts, venues, and COI wording.

Arlington is not just a suburb between Dallas and Fort Worth. It is a mid-Cities construction market with residential neighborhoods, commercial corridors, public infrastructure, UT Arlington, AT&T Stadium, Globe Life Field, Six Flags Over Texas, Hurricane Harbor, Arlington Convention Center, and Texas Live! in the same local economy.

That combination affects contractor GL pricing in four ways.

First, stadium and entertainment district work can create higher severity potential. A small trip-and-fall claim on a private remodel is not the same exposure as a claim connected to a public venue, entertainment complex, or high-traffic commercial site.

Second, contracts tend to be more demanding. Venue operators, city bid packets, commercial landlords, and large project owners often require exact Additional Insured wording, Primary Noncontributory status, Waiver of Subrogation, completed operations language, and higher limits.

Third, Arlington contractors often serve a wide geography. A contractor based in Arlington may work in Tarrant County, Dallas County, Grand Prairie, Mansfield, Pantego, Dalworthington Gardens, Kennedale, and the broader mid-Cities corridor. Carriers look at the full operating footprint, not only the mailing address.

Fourth, the construction industry itself has meaningful hazard exposure. OSHA’s construction industry page identifies construction as a high-hazard industry involving alteration, repair, heavy equipment, falls, electrocution, silica dust, and other exposures. BLS construction industry data also tracks construction employment, openings, separations, and industry labor patterns that help show the size and activity level of the sector.

“In 15+ years writing Texas contractor GL, the #1 reason Arlington stadium-district and entertainment-venue COIs get rejected is not the policy, it is missing the venue operator’s exact Additional Insured + Primary Noncontributory wording. Read the schedule before you bind.”

Pascal Burke, Licensed Insurance Broker (CA #6015321, TX #3305690)

This is also why answer-engine visibility matters. Pew’s AI summary study found that users who encountered a Google AI summary clicked traditional search results less often than users who did not. For a page like this to be cited by AI Overviews and answer engines, it needs clear dollar figures, local contract context, and concise answer-ready summaries, not generic insurance copy.

Cost by coverage limit

In brief: A $1M/$2M policy is the baseline for many Arlington contractors, but stadium, venue, municipal, and larger commercial contracts may require $2M/$4M or $5M+ through umbrella or excess liability.

Most Arlington contractors start with a $1M per occurrence / $2M aggregate general liability policy, but contracts can push limits higher when the project involves a public entity, high-value venue, or large commercial owner.

Coverage structure | Common use in Arlington | Pricing impact | Notes |

|---|---|---|---|

$1M occurrence / $2M aggregate | Standard residential and light commercial contractor GL | Baseline | Common minimum for many leases, contracts, and vendor packets |

$2M occurrence / $4M aggregate | Larger commercial, venue, public works, or owner-controlled requirements | Moderate increase | May be written directly or through policy structure depending on carrier |

$1M/$2M GL plus $1M umbrella | Contractors needing extra limits over GL and auto | Moderate to higher | Umbrella pricing depends on underlying operations and auto exposure |

$5M total limits | Stadium, entertainment district, institutional, or larger commercial projects | Higher | Often built with umbrella or excess liability |

Project-specific higher limits | Large owner, GC, municipality, or venue requirement | Case-specific | Contract wording should be reviewed before binding |

TDI’s CGL guidance explains that excess liability can pay for covered losses above the CGL policy limit and that umbrella liability may sit over auto liability and CGL. For contractors, that means a venue requirement for $5M does not always mean the base GL policy itself must be $5M. It may mean $1M/$2M GL plus umbrella or excess liability, depending on the contract.

If your project owner asks for proof of general liability coverage, send the full insurance exhibit before you buy. The cost difference between a basic $1M/$2M certificate and a strict venue packet can be significant.

The 7 factors carriers use to price your policy

In brief: Carriers price Arlington contractor GL by trade, size, subcontractor exposure, job type, limits, endorsements, and loss history, not by city name alone.

Insurance carriers do not price Arlington general liability by pulling one flat city rate. They rate the actual risk. A clean interior painting contractor with two employees and no subcontractors can be a very different risk than a roofing contractor doing commercial exterior work near the entertainment district.

Pricing factor | What the carrier looks at | Arlington example | How to improve the quote |

|---|---|---|---|

1. Trade classification | Type of work performed | GC, roofer, plumber, concrete, finish trade | Use accurate class descriptions and avoid vague applications |

2. Annual revenue | Gross receipts and project size | $250K remodeler vs $2M commercial GC | Provide realistic current and projected revenue |

3. Payroll and owner role | Employee count and field exposure | Owner-only business vs crew with supervisors | Separate owner, clerical, and field payroll clearly |

4. Subcontractor costs | Insured vs uninsured subcontractors | GC using multiple trades in Tarrant County | Collect COIs from every subcontractor |

5. Project type | Residential, commercial, public, venue, or industrial | Stadium vendor packet vs single-family remodel | Provide contracts and job descriptions |

6. Limits and endorsements | $1M/$2M, $2M/$4M, AI, PNC, WOS | Entertainment venue requiring exact wording | Send insurance requirements before binding |

7. Claims history | Prior losses, open claims, and risk controls | Water damage, trip claim, completed operations issue | Explain corrective action and safety changes |

Subcontractor classification deserves special attention. TWC’s worker classification guidance warns that misclassifying employees as independent contractors can create tax penalties and added costs. From an insurance standpoint, uninsured or poorly documented subs can also affect audits, COI approval, and carrier appetite.

For general liability insurance for Texas contractors, the strongest applications usually include accurate trade details, clean subcontractor controls, realistic revenue projections, and the actual contract wording.

Arlington contract, lease, and COI requirements

In brief: Arlington contractors should treat COI wording as a contract requirement, not a paperwork detail, especially for city, venue, stadium, commercial lease, and subcontractor agreements.

Arlington contractor GL requirements usually come from contracts, not a single statewide law. A property owner, general contractor, city department, venue operator, landlord, lender, or vendor portal may require proof of coverage before work starts.

The City of Arlington vendor supplier page links to insurance requirements and standard terms for vendors, and city work may require registration through procurement systems. For private work, Arlington homeowners and commercial owners may also ask for proof of liability coverage, especially when the job involves occupied property, public access, or high-value improvements.

Common COI requirements include:

$1M per occurrence / $2M aggregate general liability limits

Products-completed operations coverage

Additional Insured status for the owner, GC, landlord, venue, or municipality

Primary and Noncontributory wording

Waiver of Subrogation

30-day notice wording if available from the carrier

Specific project or location description

Umbrella or excess liability for higher-limit contracts

Workers compensation or occupational accident proof when employees or subs are involved

Commercial auto proof for vehicles entering the site

For a practical overview, review Certificate of Insurance basics before submitting proof to a venue or owner. If the contract asks that another party be added to your policy, confirm the exact Additional Insured endorsement language before binding. If the agreement requires the insurer to waive recovery rights against a project owner or GC, confirm whether a Waiver of Subrogation is available for your class and carrier.

The biggest mistake is buying the cheapest GL policy first, then discovering the carrier cannot issue the required endorsement wording.

What general liability does NOT cover

In brief: General liability does not cover every contractor risk. Employee injuries, business vehicles, professional design mistakes, faulty workmanship, tools, pollution, cyber events, and surety obligations may require separate coverage.

General liability is foundational, but it is not a complete contractor insurance program. The III CGL guide notes that CGL generally does not cover professional errors, intentional acts, employee injuries, and certain cyber or pollution claims.

Common exclusions and gaps include:

Employee injuries, usually handled through workers compensation or occupational accident coverage

Business vehicle accidents, usually handled through commercial auto

Damage to your own work, often excluded or limited under business-risk exclusions

The cost to repair defective workmanship itself

Professional design, consulting, or engineering errors

Tools, materials, and equipment, usually handled through inland marine

Pollution, mold, or environmental losses unless specifically endorsed or separately covered

Cyber events, data breach, or payment fraud

Contractual penalties that exceed covered liability

Surety bond obligations

This matters for Arlington contractors because venue and commercial projects may ask for more than GL. A contractor entering Texas Live!, Globe Life Field, AT&T Stadium, or Arlington Convention Center vendor systems may need GL, auto, workers compensation, umbrella, and exact COI wording.

Use jobsite GL insurance as the starting point, then build the rest of the insurance program around the contract. For many general contractors, GL is only one line in a broader compliance package.

How Arlington contractors can lower GL costs without creating coverage gaps

In brief: The right way to lower GL cost is to improve risk quality, documentation, and carrier fit, not to remove the endorsements your contracts require.

The cheapest policy can become expensive if it fails a COI review, excludes your real work, or leaves completed operations underinsured. Arlington contractors should focus on making the account easier for carriers to underwrite.

Practical ways to control cost include:

Classify the work accurately. Do not call structural remodeling “handyman work” to chase a lower rate. Misclassification can create audit and claim problems.

Keep clean subcontractor records. Collect COIs, written subcontract agreements, and Additional Insured status from every subcontractor.

Separate high-risk operations. Tell the broker when roofing, structural, demolition, excavation, or hot work is occasional versus core revenue.

Send contracts before binding. Stadium, venue, municipal, and commercial owner packets may require endorsements that not every carrier offers.

Improve safety practices. Written safety rules, site controls, housekeeping, fall protection, and incident tracking can help the underwriting narrative.

Avoid lapses. Continuous coverage is easier to place than a contractor account with gaps.

Explain prior claims. A loss is not always fatal, but carriers want to know what changed afterward.

Review limits annually. Revenue growth, bigger contracts, or new venue work may require higher limits than last year.

Compare carrier appetite, not just price. A cheap quote that cannot issue the right COI is not a functional quote.

Bundle when appropriate. Some contractors can improve efficiency by coordinating GL, auto, workers compensation, inland marine, and umbrella through aligned markets.

For contractors bidding public, commercial, or entertainment district work, the contract should control the insurance conversation. If the project requires specific endorsement language, do not remove it just to save premium. That is how COIs get rejected after the job has already been awarded.

What to prepare before requesting a quote

In brief: An Arlington contractor can speed up a GL quote by sending trade details, revenue, payroll, subcontractor costs, prior losses, current policy, and any stadium or venue insurance packet upfront.

Most GL quote delays come from missing underwriting information. Before requesting pricing, gather the items below.

Quote item | What to provide | Why it matters |

|---|---|---|

Legal business name | LLC, corporation, DBA, or sole proprietor name | Needed for accurate policy and COI issuance |

Texas license or registration details | Any applicable trade, local, or state credentials | Helps match operations to carrier appetite |

Owner information | Names, experience, prior business history | Experience can improve underwriting confidence |

Business location | Arlington address and operating territory | Confirms Tarrant County, Dallas County, and nearby service area |

Trade description | Exact work performed and excluded work | Prevents incorrect classification |

Annual revenue | Last year and projected current year | Core rating basis for many contractor GL policies |

Payroll | Owner, clerical, and field payroll | Helps underwrite employee exposure |

Subcontractor costs | Insured and uninsured subcontractor totals | Affects audit, rating, and eligibility |

Prior claims | Date, amount, cause, and corrective action | Helps explain loss history |

Current policy | Declarations page and endorsements | Allows accurate comparison |

Contract requirements | Insurance exhibit, lease, bid packet, or vendor portal language | Confirms limits and endorsements before binding |

Stadium / venue vendor portal? Y/N | Identify AT&T Stadium, Globe Life Field, Texas Live!, Six Flags, Hurricane Harbor, or Arlington Convention Center exposure | Determines whether special wording or higher limits may be needed |

COI deadline | Same day, 24 hours, or future effective date | Helps prioritize carrier and servicing path |

“The fastest Arlington GL quote is the one that arrives with the contract requirements attached. If a contractor tells us the trade, revenue, subcontractor spend, loss history, and whether a stadium or venue portal is involved, we can avoid most back-and-forth before binding.”

Pascal Burke, Licensed Insurance Broker (CA #6015321, TX #3305690)

This is where Texas contractor GL requirements differ from generic small-business insurance. The risk is not only what you do. It is what your contract requires you to prove before you step on the jobsite.