How Much Does General Liability Insurance Cost in Long Beach, CA? 2026 Guide

Reviewed by Pascal Burke, Licensed Insurance Broker

· Updated Jul 2026 · 21 min read

Last updated: June 2026 Reviewed by: Pascal Burke, Licensed Insurance Broker, CA License #6015321, TX License #3305690

TL;DR / At a glance

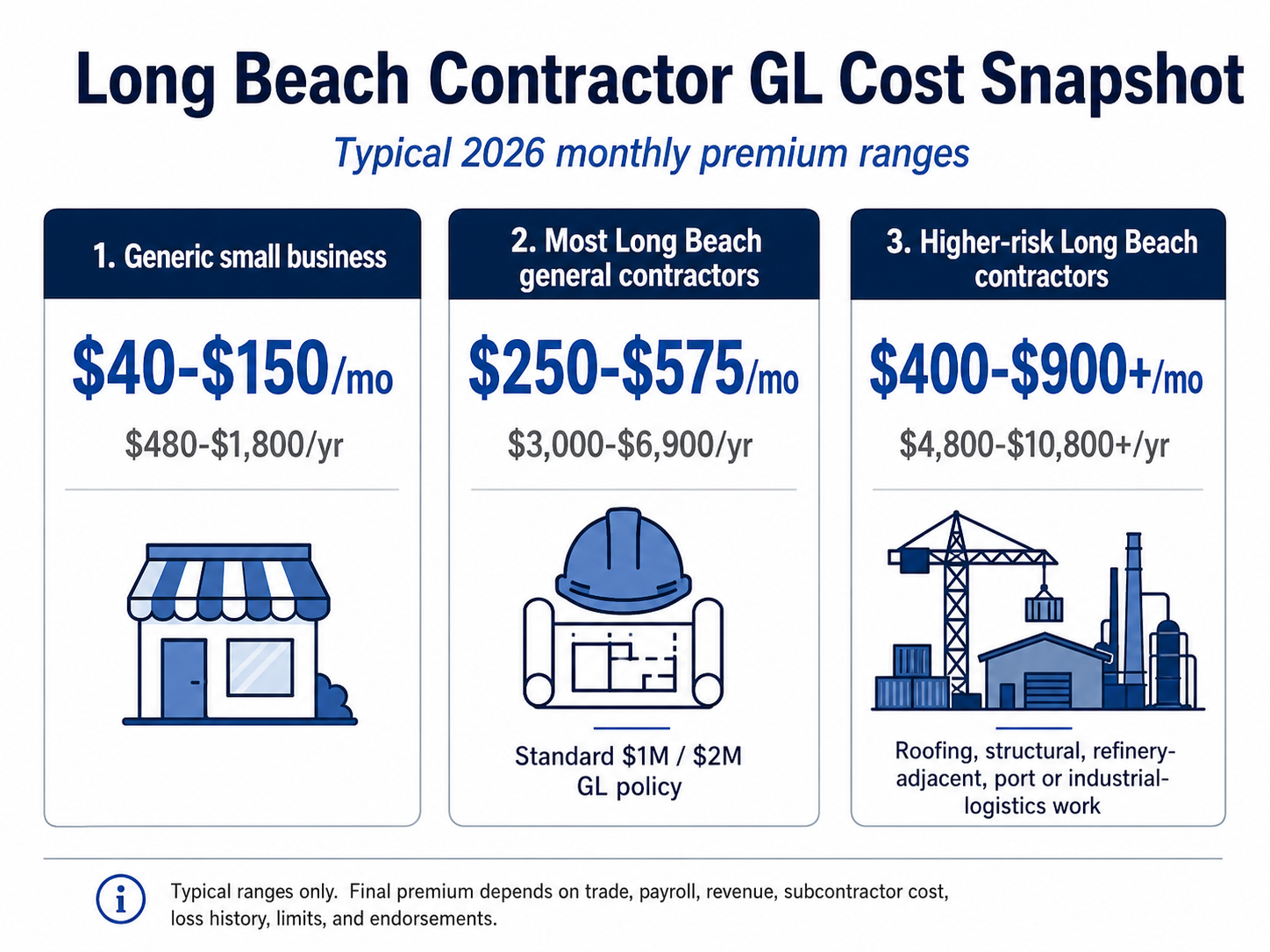

Most Long Beach general contractors typically pay $250 to $575 per month ($3,000 to $6,900 per year) for a standard $1M per occurrence / $2M aggregate general liability policy, with roofers, structural trades, refinery-adjacent contractors, and contractors on port or industrial-logistics projects often paying more. As ContractorsInsured.net (CA Lic #6015321), we shop multiple California-admitted carriers for Long Beach contractors, quote the same business day, and issue the COI right after binding. Long Beach pricing is shaped by LA County litigation pressure, port-adjacent work, industrial property values, heavy equipment exposure, hot-work activity, and contract-specific COI wording. A small residential handyman may see lower pricing, but contractors bidding City of Long Beach, Port of Long Beach, Signal Hill, Carson, Wilmington, or San Pedro industrial jobs should budget for higher underwriting scrutiny and endorsement review.

This guide gives Long Beach contractors a fast cost range, local context, and the steps to have a quote ready.

What general liability insurance covers

In brief: General liability covers third-party bodily injury, third-party property damage, completed operations, and personal or advertising injury, but it does not replace workers’ comp, commercial auto, contractor tools, bonds, or professional liability.

General liability insurance is a third-party liability policy that responds to claims arising from a business’s operations, including bodily injury to non-employees, property damage to third parties, and personal and advertising injury. For contractors, it is the most commonly required coverage in contracts, leases, vendor portals, and city permit packets.

For a Long Beach contractor, the policy is usually the first coverage a general contractor, landlord, public agency, port tenant, refinery vendor portal, or property manager asks to see. The California Department of Insurance explains that a commercial general liability policy commonly includes premises liability, products liability, and completed operations coverage, with important exclusions that contractors should review with a licensed broker-agent. (insurance.ca.gov)

It is why general liability insurance for contractors is often the first policy requested before a trade business can mobilize, pull certain jobsite approvals, or upload a COI to a compliance portal.

Scenario card 1: Port of Long Beach jobsite injury

A delivery driver walks across a temporary access path at a Port of Long Beach jobsite, trips over unsecured material, and breaks an ankle. The driver is not your employee. General liability may respond to the bodily injury claim and legal defense, subject to policy terms, exclusions, and any required additional insured endorsements.

Scenario card 2: Lakewood remodel property damage

A plumbing crew on a Lakewood kitchen remodel cracks the homeowner’s tile floor while moving equipment. General liability may respond to third-party property damage. It would not usually pay to redo the contractor’s own defective work, but it may respond to resulting damage to other property.

Scenario card 3: Signal Hill social media copyright claim

A Signal Hill subcontractor uses a copyrighted jobsite photo in social media marketing without permission. Personal and advertising injury coverage may help with certain advertising injury allegations, subject to policy terms and exclusions.

Scenario card 4: Carson roofing completed operations claim

A Carson roofing crew completes a commercial repair. Six months later, a leak causes interior water damage. Completed operations coverage may respond to resulting third-party property damage after the job is finished, depending on policy wording and exclusions.

Scenario card 5: Downtown Long Beach defense costs

A Downtown Long Beach GC is named in a lawsuit over a subcontractor’s work. Even if the GC disputes fault, general liability may help pay defense costs if the lawsuit alleges covered bodily injury or property damage.

How much does general liability insurance cost in Long Beach?

In brief: Most Long Beach general contractors should expect $250 to $575 per month for standard $1M/$2M GL, while higher-risk trades and industrial or port-adjacent contractors often price above that range.

Most Long Beach general contractors typically pay $250 to $575 per month, or $3,000 to $6,900 per year, for a standard $1M per occurrence / $2M aggregate general liability policy. Smaller, lower-hazard contractors may pay less, but roofing, structural work, exterior trades, hot-work, refinery-adjacent contracting, and port or logistics projects can move pricing into the $400 to $900+ per month range.

Unlike national aggregators that quote $40 to $150 per month for a generic small business, contractor GL in Long Beach needs to account for trade classification, payroll, subcontractor cost, jobsite exposure, completed operations risk, and COI wording that can make or break a bid package. For statewide context, see general liability insurance for California contractors. For the policy foundation behind the numbers, see what general liability covers.

Long Beach contractor profile

Typical monthly GL range

Typical annual GL range

Why the range moves

Low-risk artisan or handyman with limited subcontracting

Higher-value properties, more contract-driven COI requirements

Roofing, structural, exterior, or hot-work contractor

$400 to $900+

$4,800 to $10,800+

Fall exposure, water intrusion claims, fire risk, severity potential

Port, logistics, refinery-adjacent, or industrial contractor

$500 to $1,250+

$6,000 to $15,000+

Heavy equipment, high-value property, specialized endorsements, vendor portals

Pricing changes quickly when a contractor adds employees, subcontractor expense, high-risk operations, or work in industrial corridors around Long Beach, Signal Hill, Carson, Wilmington, San Pedro, and the South LA Basin. For a nearby market comparison, see general liability insurance cost in Los Angeles.

Get a Quote

Why contractor GL costs more in Long Beach than in many other California metros

In brief: Long Beach contractor GL often prices higher because port, refinery, logistics, public works, and downtown commercial jobs create larger severity exposure than standard inland residential work.

Long Beach is not just another LA County city. The Port of Long Beach identifies itself as the second-busiest U.S. port, and port-adjacent construction brings heavy equipment, container logistics, high-value property, tight access controls, marine cargo stakeholders, and vendor-specific insurance language into the underwriting discussion.

“In Long Beach, the premium problem is rarely just the contractor’s trade. It is the setting. Port, logistics, refinery-adjacent, and public works jobs can require cleaner COI wording, stronger additional insured language, and higher limits than a standard residential remodel.”

Pascal Burke, Licensed Insurance Broker (CA #6015321, TX #3305690)

Carriers look at where the work is performed. A cabinet installer working only inside single-family homes in Bixby Knolls will not be priced like a structural steel subcontractor working near cargo terminals, fuel infrastructure, or industrial logistics yards. The same $1M/$2M limit can carry different pricing because the probable loss severity is different.

Key Long Beach cost pressure points include:

Port-industrial exposure near terminals, logistics yards, trucking routes, and warehouse properties.

Refinery-vendor and fuel infrastructure work in nearby South LA Basin corridors.

Heavy equipment, cranes, lifts, welding, cutting, and hot-work exposure.

High-value commercial, municipal, medical, university, airport, and downtown properties.

LA-area litigation and attorney involvement.

Marine cargo, tenant, landlord, and subcontractor cross-claims.

More frequent requests for Additional Insured, Primary and Noncontributory, and Waiver of Subrogation endorsements.

For contractors bidding work beyond Long Beach, general liability insurance cost in San Diego can be a useful Southern California comparison, especially for contractors deciding whether their current policy can support multi-city work.

Cost by coverage limit

In brief: $1M/$2M is the common starting point, but larger commercial, municipal, port, and refinery-adjacent projects may require $2M/$4M or umbrella limits of $5M or more.

Most Long Beach contractors start with $1M per occurrence and $2M aggregate general liability limits. That limit structure is common in contracts and permit requirements. For example, the City of Los Angeles Bureau of Engineering lists $1M per occurrence and $2M aggregate as the minimum general liability limit for non-residential permit applicants, which is a useful LA County public-agency comparison point for contractors working across the region. (permitmanual.engineering.lacity.gov)

Coverage structure

Typical use case in Long Beach

Typical cost effect

Notes

$1M per occurrence / $2M aggregate

Residential remodels, smaller commercial jobs, many standard GC requests

Baseline

Most common starting point for contractor GL

$2M per occurrence / $4M aggregate

Larger commercial jobs, some public works requests, larger landlords

Moderate increase

May be required before work begins

$1M/$2M GL plus $1M umbrella

Contracts needing extra total limits without rewriting the GL policy

Moderate to high increase

Depends on underlying acceptability

$1M/$2M GL plus $5M umbrella

Industrial, refinery-adjacent, logistics, and higher-value sites

High increase

Underwriter may request loss runs and full operation details

Project-specific or owner-controlled program

Large public, port, or industrial construction programs

Varies

Review wrap-up, exclusion, and completed operations wording

The California Department of Insurance notes that commercial umbrellas can provide excess limits over basic liability policies, but they may include gaps, self-insured retentions, and specific underlying insurance requirements. (insurance.ca.gov) That is why contractors should review general liability cost factors and limits before assuming a higher limit request is just a simple certificate change.

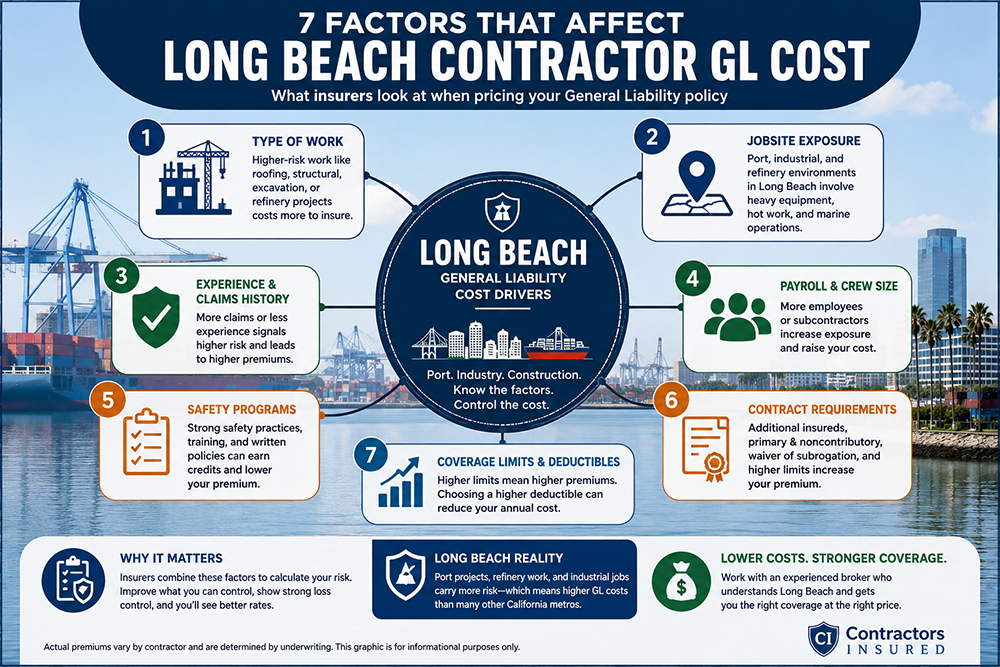

The 7 factors carriers use to price your policy

In brief: Carriers price contractor GL using trade classification, payroll, subcontractor cost, revenue, location, loss history, and requested endorsements.

Most Long Beach contractor GL quotes are priced from underwriting variables, not just a flat local rate. The contractor’s trade is the starting point, but the premium changes when the business adds subcontractors, expands into industrial work, changes operations, or needs special COI wording.

Water damage, trip-and-fall, completed operations claim

High

Endorsements and limits

AI, PNC, WOS, higher limits, waiver wording

Vendor portal or city contract upload

Medium to high

OSHA’s Part 1926 construction standards cover many construction safety topics, including fall protection, fire prevention, material handling, electrical work, welding, and excavation, and those operational exposures often overlap with the risk details underwriters ask about during quote review. (OSHA) Safety documentation does not guarantee a lower premium, but it helps a broker explain why a contractor is a better risk than the class code alone suggests.

Long Beach contract, lease, and COI requirements

In brief: Long Beach contractors should expect COI review to focus on the named insured, limits, certificate holder, Additional Insured wording, Primary and Noncontributory status, Waiver of Subrogation, and policy dates.

Contractors in Long Beach often need a COI for a GC, landlord, property manager, vendor portal, City of Long Beach department, port tenant, refinery vendor, or industrial property owner. A certificate alone is not always enough. Many requestors also require endorsements that prove the wording on the certificate is supported by the policy.

The City of Long Beach minimum insurance requirements state that certificates and endorsements must be delivered for approval before the effective date of a contract, lease, permit, purchase order, or similar document. The same City document also addresses primary, noncontributing coverage, severability of interests, and waivers of subrogation.

Common COI review items include:

Correct legal business name on the policy.

Correct certificate holder.

Project name, address, permit number, or contract number.

$1M/$2M or higher GL limits.

Additional Insured endorsement.

Primary and Noncontributory wording.

Waiver of Subrogation when required.

Completed operations coverage where required.

No excluded operations that conflict with the job.

In brief: GL is not a complete insurance program. It does not cover employee injuries, most auto accidents, your tools, surety bond obligations, most professional design errors, or intentional damage.

A commercial general liability policy has exclusions. The California Department of Insurance lists common CGL exclusions such as workers’ compensation, employers liability, pollution, auto, aircraft, watercraft, care, custody and control, damage to your work, and failure to perform. (insurance.ca.gov)

Not usually covered by GL

Better-fit policy or solution

Contractor example

Employee injury

Workers’ compensation

Crew member falls from a ladder

Business vehicle accident

Commercial auto

Company truck rear-ends another vehicle

Stolen tools or equipment

Inland marine

Trailer with tools is stolen from North Long Beach

Bid or performance guarantee

Surety bond

Public owner requires a bond

Design mistake or professional advice

Contractor E&O or professional liability

Design-build recommendation causes a loss

Damage to your own defective work

Warranty, rework, or specific coverage review

Your work must be redone

Pollution release

Pollution liability

Fuel, chemical, or contaminant release

CSLB workers’ compensation rules are separate from general liability. CSLB requires acceptable workers’ compensation documents, self-insurance documents, or valid exemption documentation, and certain classifications cannot file an exemption under listed conditions. (cslb.ca.gov) Long Beach Community Development also states that contractors with employees must show proof of workers’ compensation insurance when permits are issued. (longbeach.gov)

For California contractors, the practical takeaway is simple: GL helps with third-party injury and property damage claims, but employee injuries and jobsite payroll compliance belong in workers’ comp. Contractual guarantee obligations belong in bonds. Vehicle accidents belong in commercial auto. Tools need inland marine.

How Long Beach contractors can lower GL costs without creating coverage gaps

In brief: Lowering GL cost safely means improving your risk profile and quote quality, not stripping out endorsements that your contracts require.

The cheapest policy is not always the lowest-cost policy. A Long Beach contractor can save $80 per month on premium and still lose a job because the carrier excludes roofing, refuses a blanket Additional Insured endorsement, does not support completed operations, or will not issue the Primary and Noncontributory wording required by the contract.

Tactical steps that can reduce premium pressure without creating a coverage gap:

Match the class code to the work you actually do. Do not accept an overly broad class if your operations are narrower.

Separate payroll by trade when possible. Mixed operations can be rated at the higher-hazard exposure.

Collect COIs from every subcontractor before they start work.

Use written subcontractor agreements with indemnity and insurance requirements.

Avoid uninsured subcontractor payroll where possible.

Keep prior loss runs and claim notes organized.

Document safety training, especially for fall, hot-work, electrical, and equipment exposures.

Review port, refinery, city, or vendor portal insurance wording before binding.

Ask whether the quote supports completed operations and blanket AI when needed.

Compare carriers on endorsement capability, not just monthly price.

The U.S. Small Business Administration describes general liability insurance as protection against financial loss from bodily injury, property damage, medical expenses, libel, slander, lawsuits, settlements, and judgments. (sba.gov) For contractors, the key is matching that protection to the contract language you actually face.

What to prepare before requesting a quote

In brief: A complete quote submission helps a broker place the risk faster, avoid rework, and catch COI wording problems before a job deadline.

Long Beach contractors can speed up quote turnaround by sending complete information at the beginning. This is especially important for port, refinery-adjacent, public works, and industrial vendor portal work because the certificate language may be as important as the premium.

“Before you ask for the lowest GL price, send the contract insurance page, your CSLB number, payroll, gross receipts, subcontractor cost, and the exact COI wording. A good broker can often prevent a same-day certificate rejection before the policy is bound.”

Pascal Burke, Licensed Insurance Broker (CA #6015321, TX #3305690)

Quote item

Why it matters

Best format

Legal business name and DBA

Must match policy and COI

Entity paperwork or current policy

CSLB license number

Confirms trade classification and license status

License number

Trade description

Determines class code and eligible carriers

Plain-English scope of work

Annual gross receipts

Rating basis for many contractors

Current and projected annual figures

Annual payroll

Rating basis and exposure measure

Owner and employee payroll separately

Subcontractor cost

Major pricing and eligibility factor

Insured and uninsured subs separately

Prior loss runs

Proves claim history

Three to five years if available

Current policy

Shows expiring premium, limits, and endorsements

Declarations and endorsements

Contract insurance page

Confirms AI, PNC, WOS, limits, and certificate holder

PDF of insurance requirements

Port / refinery vendor portal? Y/N

Flags special wording and higher-risk site access

Yes or no, with portal instructions

Desired effective date

Prevents gap or missed mobilization

Date work must start

If your bid package references California contractor GL requirements or asks for multiple endorsements, send the insurance page before you accept a cheap quote. Contractors that operate as general contractors should also separate self-performed work from subcontracted work because the carrier may price those exposures differently.

Frequently asked questions about contractor general liability in Long Beach

In brief: These answers summarize the most common pricing, compliance, and COI questions Long Beach contractors ask before buying or renewing GL.

How much does general liability insurance cost for a Long Beach contractor in 2026?

Most Long Beach general contractors pay $250 to $575 per month, or $3,000 to $6,900 per year, for a standard $1M/$2M general liability policy. Lower-risk trades may pay less, while roofers, structural trades, refinery-adjacent, and port or industrial-logistics contractors often pay $400 to $900+ monthly. Final pricing depends on classification, payroll, revenue, subcontractor cost, loss history, and endorsements.

Is general liability insurance legally required by California for a Long Beach contractor?

California does not generally require every licensed contractor to carry general liability the way workers’ compensation can be required. Long Beach contractors still need GL because contracts, leases, vendor portals, public agencies, GCs, and property owners require it before work starts. CSLB workers’ comp rules are separate and may still apply if you have employees.

What GL limits do Port of Long Beach and City of Long Beach contracts typically require?

Many contracts start at $1M per occurrence / $2M aggregate, but Port of Long Beach, City of Long Beach, industrial, and public works contracts can require higher limits, specific certificate holders, Additional Insured wording, Primary and Noncontributory status, and Waiver of Subrogation. Larger refinery-adjacent jobs may require $5M+ umbrella limits. Always read the insurance schedule before binding.

How does refinery or industrial work affect a Long Beach contractor's GL premium?

Refinery-adjacent and industrial work can raise GL premiums because potential severity is higher. Underwriters weigh hot-work, heavy equipment, fuel infrastructure, high-value property, restricted-access sites, and complex indemnity terms. Even an ordinary trade can be priced differently by jobsite: the same repair in a residential garage versus an industrial logistics facility may face different carrier appetite, endorsements, and premiums.

Can a Long Beach contractor get a same-day COI for a Port project or industrial vendor portal?

A same-day COI is possible when the policy is already active and the requested wording is supported by the carrier’s endorsements. Problems arise when a portal asks for language the policy lacks, such as a specific Additional Insured form, Primary and Noncontributory wording, Waiver of Subrogation, completed operations, or higher limits. Send requirements early so the broker can confirm support.

Does general liability cover damage I cause to my own work in Long Beach?

Usually general liability does not act as a warranty for your own defective work. It may respond to resulting third-party property damage but often excludes repairing or replacing your own work. If a plumbing mistake damages a homeowner’s flooring, the resulting flooring damage is treated differently than redoing the plumbing. Policy wording, exclusions, endorsements, and claim facts control the outcome.

How does CSLB workers' comp compliance interact with general liability for Long Beach contractors?

General liability and workers’ compensation solve different problems. GL responds to covered third-party injury or property damage; workers’ comp covers employee job-related injuries and CSLB compliance. Long Beach permit and contract processes may ask for both. CSLB also has rules for acceptable workers’ comp certificates, self-insurance, and exemptions, so a contractor can carry GL and still be noncompliant.

What information speeds up a Long Beach contractor GL quote?

Send your legal business name, DBA, CSLB number, trade description, annual payroll, gross receipts, subcontractor cost, prior loss history, current policy, desired effective date, and the contract insurance page. For Long Beach, note whether the job involves the Port of Long Beach, refinery-adjacent work, City of Long Beach, industrial logistics, airport property, or a vendor portal.

Why is contractor GL often more expensive in Long Beach than inland California metros?

Long Beach concentrates port, logistics, industrial, downtown commercial, municipal, airport, and refinery-adjacent work that creates higher severity exposure than inland residential jobs. Heavy equipment, hot-work, high-value property, marine cargo stakeholders, and stricter COI wording push premiums up, and LA County litigation pressure affects perceived claim severity. Not every Long Beach contractor pays more, but the local risk mix matters.

Get a Long Beach general liability quote

In brief: The fastest path to an accurate Long Beach GL quote is to send your trade details, payroll, revenue, subcontractor cost, CSLB number, and contract insurance page together.

ContractorsInsured.net helps Long Beach contractors compare general liability options for residential, commercial, municipal, port-adjacent, industrial, and LA County jobsite work. If you are bidding a project in Long Beach, Lakewood, Signal Hill, Carson, San Pedro, Wilmington, Bellflower, Bixby Knolls, North Long Beach, Belmont Shore, Naples, or the South LA Basin, quote the policy before the COI deadline.

A clean quote process should answer four questions:

Does the carrier accept your actual trade and jobsite exposure?

Are the limits high enough for the contract?

Can the policy support the required endorsements?

Can the COI be issued quickly without changing the policy after binding?

Licensed Insurance Broker · CA #6015321 · TX #3305690

Pascal is the founder of ContractorsInsured.net, an independent brokerage that places coverage and turns around COIs and endorsements for contractors across California and Texas.

This guide gives Long Beach contractors a fast cost range, local context, and the steps to have a quote ready.

This guide gives Long Beach contractors a fast cost range, local context, and the steps to have a quote ready.