By Pascal Burke, Licensed Insurance Broker (CA License #6015321 / TX License #3305690), Founder of ContractorsInsured.net Last updated: [05/14/2026]

Editorial note: This article is educational and intended for contractors and the professionals who advise them. ContractorsInsured.net is a licensed insurance brokerage (CA License #6015321; TX License #3305690), not a law firm or claims adjuster. Premium audit outcomes generally depend on the specific carrier, audit findings, applicable rating bureau rules (WCIRB in California, NCCI in most other states), and the contractor’s records. Always confirm specific audit responses with your broker, the auditor, and qualified counsel or your CPA before disputing or paying an audit bill.

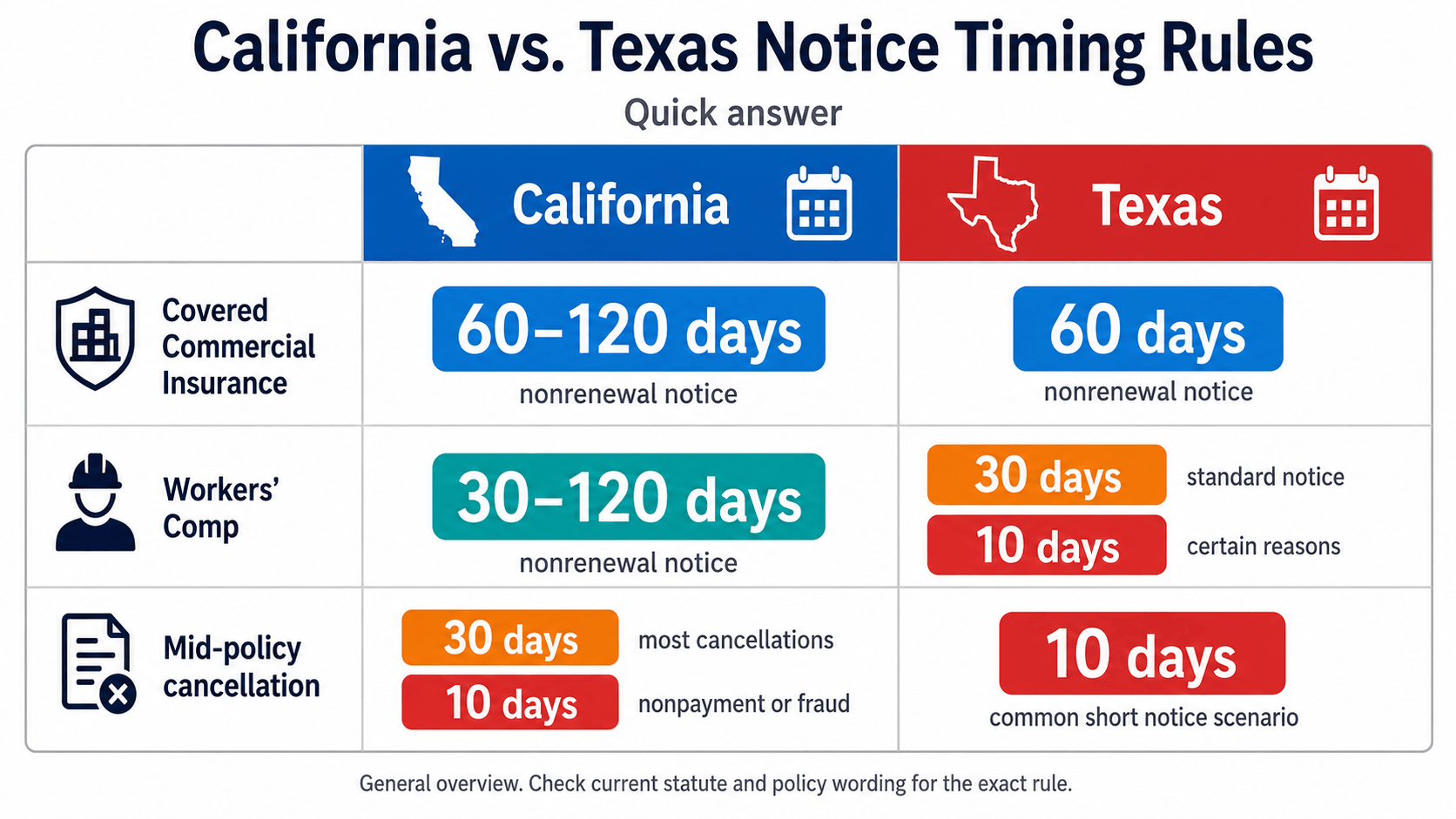

- Day 1: Read the notice carefully. In California, commercial insurance non-renewal notices generally must be sent at least 60 days but not more than 120 days before the policy ends, and the notice must include the reason for non-renewal. Workers’ compensation non-renewal notices have a separate California rule: 30 to 120 days before the policy ends. (California Legislative Information)

- Day 2: Request your loss history in writing. For California GL, commercial auto, umbrella, and other covered commercial policies, use California Insurance Code §679.7. For California workers’ comp, use California Insurance Code §11663.5. Both statutes require the report within 10 business days when the policy is canceled or non-renewed. (California Legislative Information)

- Day 7: Send a new broker the non-renewal notice, declarations pages, loss runs, audit reports, experience mod worksheet, license details, and current COIs. A replacement application is only as strong as the documentation behind it.

- Day 14: Review replacement quotes. After non-renewal, expect underwriters to ask more questions, request more loss detail, and quote tighter terms. Some accounts will need surplus-lines options.

- Day 30: Pick the replacement carrier and bind coverage before the old policy expires. A one-day workers’ comp lapse can suspend a California contractor license when coverage is required. CSLB states workers’ comp coverage must be continuous and failure to maintain it results in license suspension. (CSLB)

- Day 45: File new certificates with CSLB, GCs, owners, city registration offices, and any prequalification platforms. Update Additional Insured, Primary and Noncontributory, and Waiver of Subrogation endorsements where needed.

- Day 60+: Fix the reason the non-renewal happened. That usually means premium audit cleanup, class-code review, claim reserve review, mod management, subcontractor controls, or safety documentation.

Just received a non-renewal notice? Call ContractorsInsured at 949-522-3284. We’ll review the notice with you on the phone and tell you what the timeline and replacement options look like.

not to renew at the end of the policy period as long as it follows the notice rules, gives the required timing, and states the reason when the law requires it.

California is the more structured state for notice timing. For covered commercial insurance policies, California Insurance Code §678.1 says the insurer must give written non-renewal notice to the producer of record and named insured at least 60 days but not more than 120 days before the end of the policy period. The statute also says the notice must include the reasons for non-renewal, and if notice is late, the policy continues for 60 days after notice is given with no change in terms or conditions. (California Legislative Information)

California workers’ comp uses a separate rule. Insurance Code §11664 applies only to workers’ compensation policies and requires written non-renewal notice at least 30 days but not more than 120 days before the end of the policy period, with reasons for the non-renewal. If timely notice is not given, the policy continues for 60 days after notice at the same premium rate. (California Legislative Information)

Texas is less uniform for contractor package policies, but the same practical rule applies: read the policy and notice. Texas Insurance Code Chapter 551 includes commercial liability and commercial property cancellation and non-renewal rules, and Texas workers’ comp has its own notice framework. TDI’s workers’ comp review checklist says workers’ comp policyholders generally receive at least 30 days notice of cancellation or nonrenewal, or 10 days for listed reasons such as nonpayment, fraud, payroll misrepresentation, or increased hazard. (statutes.capitol.texas.gov)

A lawful non-renewal does not mean you are out of options. It means the next move is placement, documentation, and speed.

REASONS FOR NON-RENEWAL Quick answer:

Most contractor non-renewals come from claim activity, audit problems, high experience modification, class-code appetite changes, nonpayment, operational changes, or the carrier leaving a contractor segment.

Non-renewal feels personal. Sometimes it is not. A carrier can leave a class of business, reduce its roofing appetite, stop writing a type of residential exposure, or pull back from a state. In those cases, the non-renewal is not really about your company. You still have to replace the coverage.

Other times, the reason is specific to your account.

Reason on the notice | Likely root cause | Fix on the new application |

Loss experience or claims | Multiple claims, one severe loss, or high loss ratio | Provide loss runs, claim narratives, corrective actions, and safety changes |

High experience mod | Losses or payroll/class-code data pushed the mod above carrier appetite | Review the worksheet and explain what is being corrected |

Nonpayment or audit balance | Audit invoice, final audit dispute, or unpaid premium | Resolve or document the audit issue before shopping |

Class of business no longer written | Carrier exited roofing, demolition, high-risk residential, or another class | Use a broker with access to active contractor markets |

Operations changed | You added solar, hot work, subcontracting, waterproofing, or structural work | Break down operations by percentage and explain controls |

Carrier market withdrawal | Carrier is reducing or exiting a state/class | Document that it was market-driven, not performance-driven |

No specific detail | Notice is vague or not helpful | Request loss history and ask underwriting for clarification |

The replacement application should not hide the non-renewal. It should explain it. “Carrier exited California roofing” is very different from “three open claims and unpaid audit premium.” Underwriters know the difference.

For audit-related non-renewal, read what to do if a workers’ comp audit just hit you. For high-mod issues, see how to lower your experience modification rate.

NOTICE TIMING In California, commercial GL, property, auto, umbrella, and package policies often give you a 60 to 120 day window. California workers’ comp gives 30 to 120 days. Texas timing depends on the policy type and reason, but workers’ comp commonly uses 30 days or 10 days for specific cancellation reasons.

Start with the effective date on the notice. That is the date that matters.

State and notice type | Timing rule or practical window | What controls |

California covered commercial insurance non-renewal | 60 to 120 days before policy end | California Insurance Code §678.1 |

California covered commercial insurance late notice | Policy continues 60 days after notice | California Insurance Code §678.1 |

California workers’ comp non-renewal | 30 to 120 days before policy end | California Insurance Code §11664 |

California workers’ comp late notice | Policy continues 60 days after notice at same premium rate | California Insurance Code §11664 |

California commercial mid-policy cancellation after 60 days in force | Limited to statutory grounds | California Insurance Code §676.2 |

Texas workers’ comp cancellation or nonrenewal | Generally 30 days, or 10 days for listed reasons | Texas Labor Code / TDI checklist |

Texas GL, property, package, auto | Policy form and Texas Insurance Code rules | Policy notice and carrier letter |

California commercial cancellation after the policy has been in force more than 60 days is more restricted than end-of-term non-renewal. California Insurance Code §676.2 lists the grounds for cancellation after that point, including nonpayment, fraud, materially increased risk, failure to implement agreed loss-control requirements, and similar statutory reasons. (California Legislative Information)

The practical rule is simple: do not use the whole notice period. Treat the first two weeks like the rescue window. collect the documents a new broker needs, and send the loss-history request immediately. Do these four things tonight or tomorrow morning.

1. Circle the expiration or cancellation date

Write down the exact date and time coverage ends. Put calendar reminders 45, 30, 14, and 7 days before that date.

2. Identify which policy is affected

Do not assume all policies are affected. The notice may apply to workers’ comp only, GL only, commercial auto only, umbrella only, or a package policy.

3. Pull the broker submission file

A replacement broker needs:

- non-renewal or cancellation notice

- current declarations pages

- current policy forms if available

- loss runs or loss history

- last two workers’ comp audits

- current experience mod worksheet

- payroll by class code

- vehicle schedule

- driver list

- subcontractor controls

- CSLB license number for California

- Texas city registrations if applicable

- current contracts with insurance requirements

- active COIs and endorsements

4. Send a written loss-history request

For California commercial policies, use Insurance Code §679.7. For California workers’ comp, use Insurance Code §11663.5. Both require a premium and loss history report within 10 business days when the policy is canceled or non-renewed. (California Legislative Information)

This is the document underwriters want. It is much stronger than a contractor saying, “We only had one bad claim.” premium, claims, paid losses, reserves, and loss experience. It lets a new carrier see what actually happened instead of guessing.

California has two useful loss-history statutes for contractors.

California Insurance Code §679.7 applies to covered commercial insurance policies, other than professional liability, and requires the insurer to provide premium and loss history for the account’s tenure or the three-year period ending with the inception of the current policy period, whichever is shorter, plus current-period loss experience if the policy is canceled, non-renewed, requested within 60 days before renewal, or another listed trigger applies. The report must be provided within 10 business days. (California Legislative Information)

California Insurance Code §11663.5 applies only to workers’ compensation insurance. It requires similar premium and loss history, plus current loss experience, when a workers’ comp policy is canceled or non-renewed, requested within 60 days before renewal, or another listed trigger applies. It also requires the report within 10 business days. (California Legislative Information)

Why does this matter?

Because replacement underwriters do not like mystery. If the non-renewal was driven by one large claim, a bad subcontractor year, or a claim that is now closed, the loss-history report helps tell that story. If the account is genuinely deteriorating, the report reveals that too.

Either way, the application becomes more credible. in your trade and state. The broker should shop admitted and surplus-lines options where appropriate, disclose the non-renewal honestly, and submit a clean narrative with documentation.

After non-renewal, the biggest mistake is sending a thin application.

A good replacement submission includes:

- The non-renewal notice

- Loss-history report or loss runs

- Current declarations

- Expiring premium

- Payroll by class code

- Experience mod worksheet

- Four years of loss runs if available

- Audit reports

- Vehicle schedule and driver list

- Description of operations

- Percent subcontracted

- Safety program summary

- Corrective actions after claims

- Current COI requirements

- Desired effective date

The narrative matters. Underwriters want to know whether the non-renewal is a market issue, one-time loss, unpaid audit, class-code problem, or ongoing claim pattern.

Expect replacement coverage to cost more if the non-renewal is performance-driven. For some contractors, that means higher premium, higher deductibles, more exclusions, or a surplus-lines carrier. For others, especially where the carrier simply exited a class, replacement can be more manageable.

ContractorsInsured places workers’ compensation insurance for contractors, general liability insurance for contractors, commercial auto insurance for contractor vehicles, and supporting coverage for roofers, GCs, and plumbers in California and Texas.

We can start with the notice. Get replacement coverage after non-renewal or call 949-522-3284.

comp coverage must be continuous, and failure to maintain coverage will result in license suspension. Any work performed while the license is suspended is considered unlicensed. (CSLB)

Do not treat a workers’ comp lapse as an accounting issue. In California, it can become a license issue.

This matters for:

- C-39 roofers

- C-8 concrete contractors

- C-20 HVAC contractors

- C-22 asbestos abatement contractors

- C-61/D-49 tree service contractors

- any contractor with employees

- contractors whose GC contract requires continuous workers’ comp proof

CSLB says coverage must be continuous and the suspension is lifted once acceptable proof of coverage is received and processed. It also states that work performed while suspended is considered unlicensed. (CSLB)

Coverage issue | Likely practical consequence |

Workers’ comp certificate not replaced before expiration | CSLB suspension risk if WC is required |

Work performed while suspended | Treated as unlicensed work by CSLB |

GC checks license during gap | Project compliance problem |

Renewal occurs during gap | License renewal issue |

Employee work occurs uninsured | Potential Labor Code, CSLB, and penalty exposure |

California Business and Professions Code §7125.4 also now carries significant penalties for false exemptions or employing workers without required workers’ comp coverage: $10,000 minimum for sole owners, $20,000 minimum for entities, and up to $30,000 for later violations. (California Legislative Information)

For the full California framework, read California workers’ comp compliance under SB 216, SB 1455, and SB 291.

TEXAS CONTRACTOR RISK

Texas does not have a CSLB equivalent for general contractors, but an insurance lapse can still stop permits, breach contracts, block public work, and create workers’ comp or non-subscriber problems.

Texas risk is usually contract-driven.

A lapse can affect:

- GC prequalification

- city registration

- building permits

- public projects

- project payments

- equipment financing

- commercial auto requirements

- owner-controlled or contractor-controlled insurance programs

- jobsite access

- workers’ comp subscriber status

Texas workers’ comp has its own cancellation and nonrenewal notice rules. TDI’s workers’ comp checklist says policyholders generally receive at least 30 days notice for cancellation or nonrenewal, or 10 days notice for listed reasons such as nonpayment of premium, fraud, payroll misrepresentation, increased hazard, or commissioner determination. (Texas Department of Insurance)

For public work, Texas workers’ comp requirements can be stricter than private work. For the broader Texas choice between full workers’ comp and non-subscriber status, read the Texas non-subscriber vs. workers’ comp decision guide. For city registration consequences, see Texas contractor registration by city.

A single non-renewal is usually manageable with documentation. Multiple non-renewals, unpaid premium, audit disputes, and recent severe claims make placement harder.

Most commercial applications ask whether coverage has been canceled, non-renewed, or declined in the last three to five years. Answer truthfully.

The impact depends on why it happened.

Situation | Market reaction |

Carrier exited class or state | Usually manageable with proof |

One large claim, now closed | Manageable with claim narrative |

Repeated claim frequency | Harder, may need higher premium or deductible |

High experience mod | Harder until mod improves |

Unpaid audit premium | Serious barrier until resolved |

Prior cancellation for nonpayment | Underwriters will ask for explanation |

Second non-renewal in 5 years | Much harder placement |

A clean explanation helps. A hidden non-renewal hurts.

The path back is usually two or three clean renewal cycles, better documentation, fewer claims, paid audits, mod improvement, and a broker who starts renewal early.

Sometimes, but it is rarely the fastest solution. If the notice is late, defective, discriminatory, or factually wrong, a complaint or review may be appropriate. If the carrier simply no longer wants the risk at renewal, replacement coverage is usually the practical path.

California gives policyholders useful procedural protections. The notice must be written, timely, and include reasons. If the notice is late under §678.1 for covered commercial insurance, the policy continues for 60 days after notice. Workers’ comp has a similar continuation rule under §11664. (California Legislative Information)

California cancellation notices also must be written and include the grounds relied upon, and certain notices must tell the policyholder they may have the matter reviewed by the Department of Insurance. (California Legislative Information)

For Texas, TDI can help with insurance complaints against companies, agents, and adjusters. TDI says its Help Line is available Monday through Friday and that consumers can file complaints through its complaint process. (Texas Department of Insurance)

Still, the first priority is replacement coverage. Fighting the notice does not automatically give you a good policy, a competitive price, or a COI your GC will accept.

LOSS-HISTORY REQUEST

Send this request in writing immediately. Use §679.7 for California commercial lines and §11663.5 for California workers’ comp. For Texas, request equivalent loss runs and premium history under the carrier’s normal policyholder service process.

[Contractor letterhead]

[Date]

[Carrier name]

Attn: Underwriting Department / Customer Service

[Carrier address or email]

Re: Policy No. [policy number]

Insured: [contractor business name]

CSLB License No. [number] / Texas City Registration No. [number]

Non-Renewal Notice dated [date]

To Whom It May Concern:

This letter is a formal request for a complete premium and loss history report for the above-referenced policy and any predecessor policies issued by [carrier name] to [contractor business name].

For California commercial insurance lines other than workers’ compensation, this request is made under California Insurance Code §679.7. For California workers’ compensation insurance, this request is made under California Insurance Code §11663.5. For Texas policies, please provide equivalent loss runs, premium history, paid loss, reserve, and claim status information available under your policyholder service procedures.

Please include:

- Premium charged for each of the past three policy years

- Total losses incurred for each policy year

- Paid losses and outstanding reserves

- Loss ratio by year, if available

- Open and closed claim count by year

- Claim numbers, claim dates, and claim descriptions

- Current policy-period loss experience

- Any notes identifying catastrophic or non-catastrophic losses

Please send the report by email to [your email] and copy my broker:

ContractorsInsured.net

669 Peachy Canyon Cir #204

Las Vegas, NV 89144

info@contractorsinsured.net

949-522-3284

California Insurance Code §679.7 and §11663.5 require the applicable report to be provided within 10 business days after a qualifying written request. Thank you for your prompt response.

Sincerely,

[Owner name and title]

This template is a starting point. Adapt it to your facts. If the non-renewal involves a dispute, a large unpaid balance, claim litigation, or regulatory issue, consult a licensed attorney.

ONE-WEEK ACTION PLAN

Start replacement placement now. Do not wait for the current broker to “see what happens.” Every day matters.

Use this one-week plan.

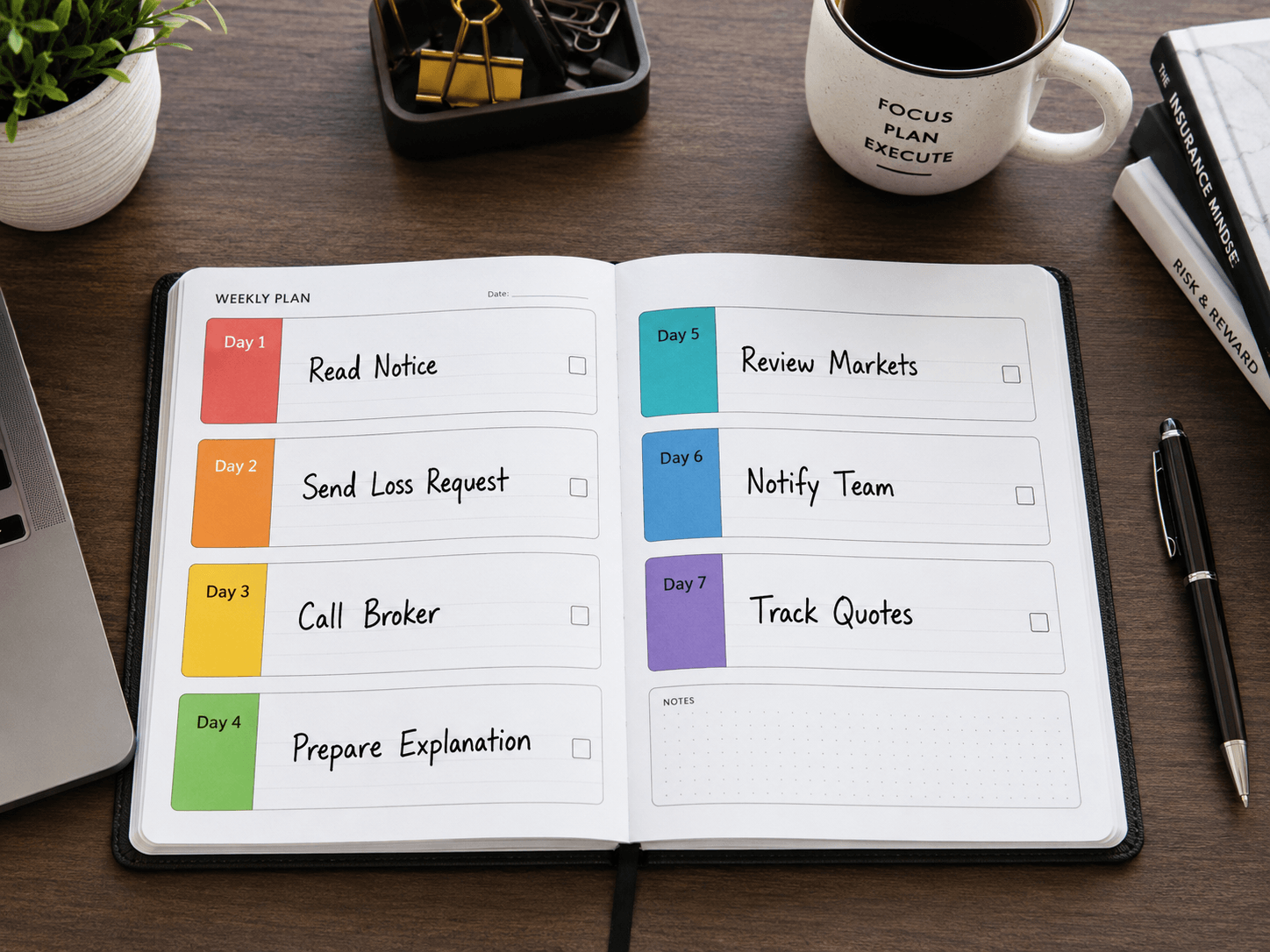

Day 1

Read the notice. Confirm the policy, expiration date, reason, and whether it is non-renewal, cancellation, or conditional renewal.

Day 2

Send the loss-history request. Pull declarations, audits, loss runs, mod worksheet, license details, and current COIs.

Day 3

Call a contractor-focused broker. Send the full submission package, not just the notice.

Day 4

Prepare a one-page explanation of the non-renewal. Include corrective actions, safety changes, audit payments, claim closures, subcontractor controls, and operational changes.

Day 5

Review market strategy. Ask which admitted markets, surplus-lines markets, workers’ comp carriers, and package options are being approached.

Day 6

Notify key internal people. Your office manager, controller, project manager, and estimator need to know a new COI may be coming.

Day 7

Track quote status. If no markets have responded or the broker has submitted to only one carrier, get a second broker involved.

We place contractor coverage in California and Texas across multiple contractor markets. Send us the notice, loss history, declarations, audits, mod worksheet, and license verification. Get replacement coverage after non-renewal or call 949-522-3284.

Technically, non-renewal happens at the end of the policy period. Mid-policy termination is cancellation. Cancellation has different rules and is usually more restricted after a policy has been in force for a certain period.

Cancellation ends the policy before the expiration date. Non-renewal means the carrier is not offering the same coverage for the next term. Conditional renewal means the carrier will renew only with changed terms, limits, deductibles, coverage, or pricing.

CSLB says workers’ comp coverage must be continuous and failure to maintain coverage results in license suspension. Work during suspension is considered unlicensed. (CSLB)

No. A COI is only useful while the policy is active. Once the policy expires or is canceled, the certificate does not create coverage.

There is not one universal public “non-renewal record,” but applications ask about cancellations, non-renewals, and declinations. You must answer truthfully.

Sometimes. It depends on trade, losses, payroll, class code, operations, and carrier appetite. Many hard-to-place contractors, especially roofers, may still need surplus-lines GL.

Higher pricing after non-renewal is common. Review deductibles, limits, exclusions, payroll, class codes, vehicle schedules, and unused coverage. Do not cut required coverage just to hit a lower number.

Usually, wait until you have a replacement plan unless the contract requires immediate notice. Once replacement coverage is bound, send updated COIs and endorsements before the old policy expires.

Yes. A single severe claim can move an account outside a carrier’s underwriting appetite, especially in roofing, construction defect, auto fleet, or workers’ comp-heavy accounts. A clean claim narrative can help replacement underwriters understand whether it was a one-off event.

Timing depends on the trade, loss history, payroll, class codes, vehicle schedule, and why the non-renewal happened. We can usually begin marketing quickly once the notice, loss history, declarations, audits, and mod worksheet are ready. Call 949-522-3284 or get a quote.

Reviewed by Pascal Burke, licensed insurance broker, CA Lic# 6015321 and TX Lic# 3305690. Pascal founded ContractorsInsured in 2017 to help contractors get insured, meet bid and licensing requirements, manage certificates, and recover from preventable coverage problems before they turn into lost work.

Last reviewed: May 13, 2026

Compliance disclaimer

This article is general information for California and Texas contractors. It is not legal advice, insurance advice, or a coverage determination. Non-renewal, cancellation, loss-history rights, CSLB consequences, Texas notice rules, and replacement-market options depend on policy language, state law, carrier procedure, claim history, payment status, and the specific facts of the notice. Where a notice, dispute, cancellation, or unpaid premium balance could materially affect your business, consult a licensed attorney and your insurance broker before acting.